What Will We Cover in this Annuity Review?

In this annuity review, we will be covering the following information on the Prudential Premier Retirement B / HDI (Highest Daily Lifetime) v3.0 annuity:- Product Type

- Fees

- Current Rates

- Realistic long-term expectations

- How it is used

- How it is most poorly used

Annuities can be complex. That’s where having an Annuity Investigator who loves math comes in. We make the complex, simple.

If you are considering the purchase of an annuity because you would like to build up your savings on a tax-deferred basis – and you are also seeking a lifetime income in retirement – then the Prudential Premier Retirement B Highest Daily Lifetime v3.0 annuity could be a viable option for you. But, prior to moving forward with a long-term commitment to this (or any other) annuity product, it is important that you know how the annuity works and what benefits it may be able to offer you as versus other annuity alternatives that are available to you. In the case of variable annuities, you will typically find that these financial vehicles will do some things well, and other things not so well. Generally, variable annuities have a focus on growing assets, based on underlying market performance. However, these products aren’t generally known for being the best at providing a reliable stream of income in retirement. One of the key reasons for this is the fact that variable annuities present much more risk to the insurance companies that offer them, as well as the consumers who purchase them. So, knowing what you can (and can’t) anticipate before you get into one of these products is essential, as they can be quite expensive to get out of if you change your mind down the road. This is where we come in.Annuity And Retirement Income Planning Information That You Can Trust

If you’ve been looking for annuity information online, then you have probably noticed that there is no shortage of “review” sites out there. In fact, you may have run across a number of different websites that claim they know all there is to know about annuities. But, while these sites may at first glance appear to be legit, the reality is that most – if not all – can best be described as copycats.

In your quest for more information about annuities, you may also have recently attended a seminar where, in return for a free lunch or dinner, the presenter offered you a plethora of details on the Prudential Premier Retirement B HDI (Highest Daily Income) annuity or some other similar product. Your attendance at that seminar may even have been the catalyst that has ultimately led you here to our website.

Possibly you have come across our Annuity Gator site for the very first time and you don’t really know what we do here. If that is the case, then please allow us to officially welcome you here. At AnnuityGator.com, we make up a team of experienced annuity professionals, and we focus on publishing the most comprehensive and unbiased annuity reviews online. We have been at this for quite some time now – far longer than our competitors have – and because of that, we have come to be known as a highly trusted source of annuity information.

Suffice it to say that here, on the website you’re on right now, you will find all of the details that you’re looking for – and possibly even some that you are not. What this means is that, because we offer complete annuity reviews, we will give you all of the pertinent details – which include not just the good, but also the bad and the ugly. Doing so, though, is really the only way to assist you with determining whether or not an annuity will truly be right for you.

So, let’s get started!

a number of different websites that claim they know all there is to know about annuities. But, while these sites may at first glance appear to be legit, the reality is that most – if not all – can best be described as copycats.

In your quest for more information about annuities, you may also have recently attended a seminar where, in return for a free lunch or dinner, the presenter offered you a plethora of details on the Prudential Premier Retirement B HDI (Highest Daily Income) annuity or some other similar product. Your attendance at that seminar may even have been the catalyst that has ultimately led you here to our website.

Possibly you have come across our Annuity Gator site for the very first time and you don’t really know what we do here. If that is the case, then please allow us to officially welcome you here. At AnnuityGator.com, we make up a team of experienced annuity professionals, and we focus on publishing the most comprehensive and unbiased annuity reviews online. We have been at this for quite some time now – far longer than our competitors have – and because of that, we have come to be known as a highly trusted source of annuity information.

Suffice it to say that here, on the website you’re on right now, you will find all of the details that you’re looking for – and possibly even some that you are not. What this means is that, because we offer complete annuity reviews, we will give you all of the pertinent details – which include not just the good, but also the bad and the ugly. Doing so, though, is really the only way to assist you with determining whether or not an annuity will truly be right for you.

So, let’s get started!

Prudential Premier Retirement B HDI v3.0 Variable Annuity at a Glance

| Product Name | Premier Retirement B HDI v3.0 |

|---|---|

| Issuer | Prudential |

| Type of Product | Variable Annuity |

| S&P Rating | AA- |

| Phone Number | (888) 778-2888 |

| Website | https://www.annuities.prudential.com/investor/hd |

Opening Thoughts on the Prudential Premier Retirement B HDI v3.0

For over a century, Prudential has been a leader in the insurance industry. Prudential Financial, Inc. companies include The Prudential Insurance Company of America, which is one of the largest life insurance companies in the United States. The company is considered to be strong and stable from a financial standpoint, with more than $1.33 trillion in assets under management, and roughly $3.7 trillion of gross life insurance in force worldwide. Through its subsidiaries, Prudential serves both individual and institutional customers in more than 40 countries. The company is ranked 1st in the “Insurance: Life and Health” category of Fortune magazine’s 2017 list of the World’s Most Admired Companies. Other rankings for Prudential include:- 2nd largest life insurer in the United States (based on total admitted assets)

- 3rd largest individual life insurance business in the United States (in terms of statutory net written premiums)

- 9th largest asset manager worldwide

- 4th largest seller of individual life insurance in the U.S. (based on recurring premiums)

Before we get into the gritty details, here are some necessary legal disclosures…

This is an independent annuity product review. It is not a recommendation to purchase or to sell an annuity. Prudential Financial, Inc. has not endorsed this review in any way, nor do we receive any type of compensation for providing this review. This annuity review is meant solely to be an independent review at the request of our readers so that they may see our perspective when breaking down the positives and the negatives of this particular annuity. Prior to committing to the purchase of any type of insurance and/or investment vehicle, it is critical that you do your own due diligence, and that you also talk with a properly licensed professional if you have any questions that relate to your specific situation. All of the names, materials, and marks that have been used in compiling this annuity review are the property of their respective owners.How Prudential Describes the Premier Retirement B HDI v3.0 Variable Annuity Product

Prudential describes their HDI – or Highest Daily Lifetime Variable Annuities as products that are “designed to help grow and protect your income for retirement while ensuring that it lasts a lifetime.” The company states that this is the only annuity benefit available that locks in highs daily and immediately starts to grow your retirement income at an annual compounded rate for the first ten years, or until you take your first guaranteed income withdrawal (which is called a Lifetime Withdrawal) – whichever comes first. This annuity is allegedly designed to do the following things:- Create guaranteed lifetime income for retirement

- Increase retirement income in up markets, while protecting it through market downturns

- Gain access to professionally managed investment portfolios

- Provide a guaranteed death benefit for your beneficiaries

- Traditional – This strategy offers management that is based on longer-term views of capital markets.

- Tactical – These portfolios offer management that is based on short-term views of capital markets.

- Quantitative – The quantitative portfolios offer a disciplined, quantitative approach to portfolio management.

- Alternative – The alternative portfolios offer traditional and non-traditional investments, which can be less correlated to the market.

How a Financial Advisor Might “Pitch” this Annuity

Because the Prudential Premier Retirement B HDI v3.0 product is a variable annuity with some unique benefits, it is likely that a financial advisor may tout the fact that you can essentially “customize” your investment strategy, while at the same time have more security in terms of future income. Some financial advisors might use the term “hybrid annuity” when offering the Prudential Premier Retirement B HDI product – which is really a marketing term some people have created to explain an annuity that provides growth, access to your money, and guaranteed income stream – all packaged into one annuity. While many of these features outlined above are true, this annuity (nor any financial vehicle) is perfect. Meaning, it may make sense to buy this type of an annuity when used correctly, but it does have its limitations just like any other financial strategy. One of the biggest concerns I have about variable annuities is that there are some agents that misrepresent how they will actually perform for you…And that may pose a financial problem for you both now and in the future, if the product does not do what you thought it would. With that in mind, before you run out and put a large chunk of your retirement savings into this annuity, there is something important to remember…If something sounds too good to be true, it probably is. Also, to cite another old saying, there is no such thing as a free lunch. This means that annuities – and especially variable annuities – are known for the plethora of fees they charge…and the Prudential Premier Retirement B HDI v3.0 variable annuity is no exception to that “rule.” In fact, if your insurance agent or financial advisor explains this annuity accurately, you should never get the impression that you will earn more than whatever the market is returning, less about 3%, due to the costs. It can lose money (all variable annuities can), including all of it, even if riders for guaranteed income are used (in extreme cases). If bigger returns than that are part of your agent’s sales pitch – run, don’t walk, to find a more honest financial advisor. It can also be beneficial to run through numbers that are based on your personal scenario. This can easily be done by using our annuity calculator. Doing so can provide you with a more realistic expectation of this annuity’s pros and cons as they relate to your specific situation. In fact, by running the numbers through our annuity calculator, we will send you, free of charge, a much more in-depth spreadsheet that can help you in determining whether or not this is really the right annuity for you. If you’re interested in seeing the results, just let us know.What About the Fees on this Annuity Product?

If you take a close look at the prospectus, you’ll notice that provided in the product’s small print, there is a list of the various fees that you can be charged – and in this case, it’s a pretty lengthy list. For starters, there is an annual maintenance fee of $50 or 2% of the contract value, whichever is less. This is assessed annually on the annuity’s anniversary date, or upon surrender of the contract. Each year, you’ll also get hit with the following annualized insurance fees and charges:- Mortality & Expense Risk Charge – 0.70%

- Administration Charge – 0.15%

- Highest Daily Lifetime Income V3.0 – up to 2.00% per year

- Spousal Highest Daily Lifetime Income V3.0 – up to 2.00% per year

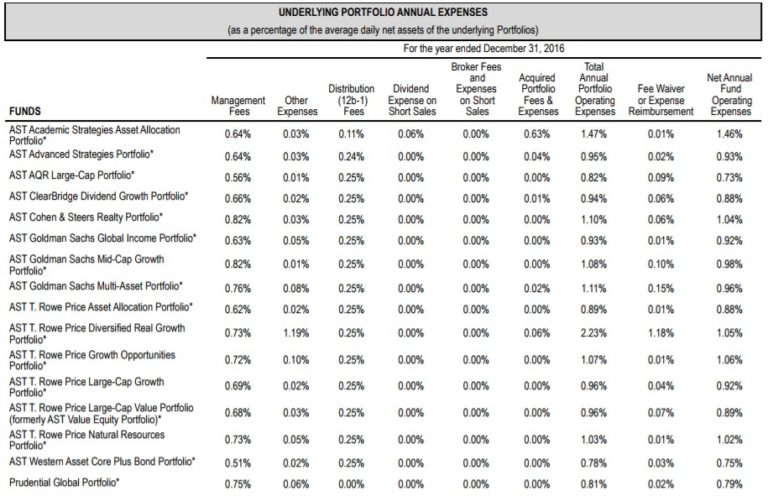

In addition to all of the above expenses, just as with other variable annuities, the fees don’t stop with just the components of the annuity product itself. Fees are also charged on the underlying portfolio investments. In the case of the Premier Retirement B HDI v3.0 from Prudential, these fees can range from 0.73% to 1.46% per year on the investments.

All of that being said, owners of the Prudential Premier Retirement B HDI V3.0 annuity could see total annual portfolio operating expenses of between 0.59% and 4.07%. So you need to ask yourself just how high the return has to be in order to generate enough to not only be in the positive but to meet or beat future inflation down the road?

In addition to all of the above expenses, just as with other variable annuities, the fees don’t stop with just the components of the annuity product itself. Fees are also charged on the underlying portfolio investments. In the case of the Premier Retirement B HDI v3.0 from Prudential, these fees can range from 0.73% to 1.46% per year on the investments.

All of that being said, owners of the Prudential Premier Retirement B HDI V3.0 annuity could see total annual portfolio operating expenses of between 0.59% and 4.07%. So you need to ask yourself just how high the return has to be in order to generate enough to not only be in the positive but to meet or beat future inflation down the road?

The Annuity Gator’s End Take on the Prudential Premier Retirement B HDI v3.0 Annuity

Where this annuity works best: This annuity could be a viable option for you, provided that you:- Are seeking the opportunity for higher return

- Have a high tolerance for risk

- Want the ability to boost your lifetime income in retirement

- Want the guarantee of principal protection

- Do not plan to use the lifetime income feature

In Summary

Annuities can be somewhat confusing products. This is especially the case with annuities that have added features – which can look really good at first glance but will also typically require you to make some tradeoffs in order to take part in the benefits. My biggest concern with this annuity (and most annuities in general), is that some consumers – and even some insurance agents and financial advisors – don’t realize what the real return potential is, and significantly over-promise what’s realistic – so it is important to be especially wary of anyone who suggests this annuity will work better than how we’ve explained it here. If the agents are being upfront and honest, you’ll notice their explanations match very closely (if not exactly) as described in this review. When that happens, you have an agent you can trust. Also, because a representative must also be securities licensed in order to offer variable annuity products, you can check the website of FINRA – the Financial Industry Regulatory Authority – to view an advisor’s background. With FINRA’s BrokerCheck, you can search via the advisor’s name, as well as by his or her firm’s name in a specific location. The only real way to anticipate how this annuity could work for you, though, is to have it tested. We can do that for you via our annuity calculator. We do this free at Annuity Gator, so just get in touch with us through our secure online form here, and we’ll use our proprietary calculator to illustrate for you what returns for your situation are likely to be. If your agent was honest with you, the numbers will match up – if not, well then you might want to reconsider who your agent is.Have Any More Questions? Did You Happen to Notice Any Mistakes on this Review?

If you feel confused about variable annuities, then don’t worry – you’re not alone. We are always happy to answer any additional questions or concerns that you have regarding the Prudential Premier Retirement B HDI V3.0 variable annuity – or any other annuity, for that matter. Just simply reach out to us through our contact form here. There are a lot of financial people out there pushing investors hard to purchase variable annuities. You need to know the real facts about annuities so you don’t make an irreversible or expensive mistake. Keep in mind that annuities are long-term contracts with surrender penalties, and for some investors, they don’t make sense at all, but for others, there could play a pivotal part of a financial plan. If you know someone that has an annuity or considering buying one, please share this variable annuity review with them. There’s a lot of conflicting information out there when it comes to annuities and their performance and my goal in writing this review was to offer you an objective review of this variable annuity. Thanks for sticking with us through this lengthy review. We realize that it went a bit long. However, our feeling is that we would much rather provide you with a bit “too much” information than with not enough. Are there any other annuities you would like to see reviewed? If so, just let us know the name or names of these products, and our team of annuity pros will get on it. Best, The Annuity Gator

Jeff Johnson

Hi,

Great commentary and I love the no nonsense approach that you gave here. But I’m a little confused with something under the “Pitch” I believe you meant to say earn not Learn here in this paragraph. “In fact, if your insurance agent or financial advisor explains this annuity accurately, you should never get the impression that you will >learn< more than whatever the".

Other than that this was great and thank you for putting out this annuity into perspective for me.

Regards,

Jeff

Annuity Gator

Hi Jeff,

We are glad to hear that you liked our review. Please pass along to others who might benefit from it.

Thank you for pointing out our typo. We have made the necessary changes.

Best,

The Annuity Gator