What will we be going over in this annuity review?

In this review of the Symetra Life Advisory Edge 5-Year Indexed Annuity, we will be going over the following information:- Annuity type

- Features and benefits

- Potential drawbacks

- Fees to look out for

- Where the annuity could work well

- Where the annuity may not be a good fit

Annuities can be complex. That’s where having an Annuity Investigator who loves math comes in. We make the complex, simple.

If you’re thinking about buying an indexed annuity, then the Symetra Life Advisory Edge 5-Year annuity may be a good fit for you – particularly if you’re seeking the opportunity for market-linked growth while also keeping your principal protected. As an added bonus, this annuity – like others – can also provide you with a reliable lifetime income, regardless of how long you may need it, regardless of what happens in the stock market. Given that, it could eliminate the worry about “running out of income before running out of time.” That being said, though, before you make a commitment to this (or any) annuity, it is extremely important that you know how it works, and what you can anticipate. Otherwise, you could be disappointed – and it could also cost you some of your account value if you end up surrendering (i.e., canceling) the annuity in the future. Throughout the past several years, fixed index annuities have become quite popular. This is due in large part to the fact that these financial vehicles can offer a guaranteed income stream during retirement. This, in turn, can give you the peace of mind in knowing that you won’t outlive your income, no matter how long you may live. Because of the increased popularity of index annuities, many insurance carriers are continuing to add new products to their proverbial shelves. Likewise, there are more financial and insurance professionals offering index annuities – but this is not necessarily a good thing. One of the main reasons for this is because, even though advisors work hard to offer the best possible information for their clients, fixed indexed annuity products are complex and have a lot of moving parts, even the insurance and financial advisors who sell them may not always be all that familiar with the intricate details about them. However, because fixed indexed annuities – or for that matter, any annuities – can oftentimes require a large percentage of your overall savings, you really need to know how the product will work because if you change your mind later and want to get out of it, you will find yourself paying a pretty hefty surrender penalty.Annuity and Retirement Income Planning Advice that You Can Actually Trust!

If this is the very first time you have visited our AnnuityGator.com website, then please allow us to personally welcome you here. We are a team of highly knowledgeable financial pros who are focused specifically on offering very in-depth and unbiased annuity reviews. We have been at this for quite a number of years now – much longer than our competitors – and because of that, we’ve become a go-to source for annuity information. If you have been in the process of compiling more information on an annuity that you’re considering purchasing, then you have more than likely come across a lot of conflicting information about these products online. This really is not surprising, though, as there is a myriad of details available about these products. There are also a wide range of opinions about them, too. While you’ve been online searching for additional annuity details, you may also have noticed that, while there are plenty of very good annuity-related websites out there, some of them will make some pretty bold claims with the goal of “luring” you in. These may include some or all of the following:- Highest annuity payouts

- Lowest fees

- Guaranteed income for life

- Top-Rated Annuity Companies

- Get an Annuity Quote Now!

The Symetra Advisory Edge 5 Fixed Index Annuity at a Glance

| Product Name | Advisory Edge 5 |

|---|---|

| Issuer | Symetra |

| Type of Product | Fixed Index Annuity |

| A.M. Best Rating | A (Excellent) |

| Phone Number | (800) 796-3872 |

| Website | https://symetra.com/ |

Opening Thoughts on the Symetra Advisory Edge 5 Indexed Annuity

Symetra is backed by more than $55 billion in assets (as of year-end 2019), and its parent company, Sumitomo Life, is one of the largest life insurance companies in Japan – and together, Sumitomo Life and Symetra have total assets of over $300 billion. Established in 1957, Symetra offers a wide array of wealth protection and retirement products, including fixed and fixed indexed annuities, as well as term, permanent, universal, bank-owned, and corporate-owned life insurance. Due to its financial strength and stability, as well as its positive reputation for paying out policyholders’ claims, Symetra is highly rated by the insurer rating agencies. In addition to earning an A from A.M. Best, these ratings include an A from Standard & Poor’s, and an A1 from Moody’s. Primarily because of the constant volatility of the stock market over the past several years, fixed index annuities have become extremely popular with investors as a way to both grow and protect principal, as well as to obtain an ongoing income in retirement. However, while these features may seem highly attractive at first glance, it is important that you look at the whole picture, because there is typically some type of “tradeoff” required.Before we get into the gritty details, here are some necessary legal disclosures…

This is an independent annuity product review. It is not a recommendation to purchase or to sell an annuity. Symetra has not endorsed this review in any way, nor do we receive any type of compensation for providing this review. This annuity review is meant solely to be an independent review at the request of our readers so that they may see our perspective when breaking down the positives and the negatives of this particular annuity. Prior to committing to the purchase of any type of insurance and/or investment vehicle, it is critical that you do your own due diligence, and that you also talk with a properly licensed professional if you have any questions that relate to your specific situation. All of the names, materials, and marks that have been used in compiling this annuity review are the property of their respective owners. For additional information on how to compare fixed annuities so that you can decide which may be the best one for you, click here in order to obtain our free annuity report.How Symetra Describes the Advisory Edge 5 Indexed Annuity

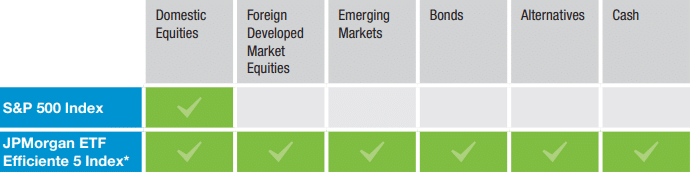

According to Symetra Life Insurance Company, the Advisory Edge annuity is a single premium fixed indexed product that helps to protect retirement savings, while two indexed account options provide opportunities for growth. This indexing allows the Advisory Edge annuity to provide higher credited interest than a traditional fixed annuity, because the interest that is earned is based on the future performance of the index(es). The indexes that are available to track with the Advisory Edge 5 annuity from Symetra include the:- S&P 500

- JPMorgan ETF Efficiente 5 Index

The amount of interest credited is subject to a “cap,” though, so if the index(es) performs well, the annuity may not attain the full return of the underlying index. In return for that, however, if the index(es) performs poorly in a given period, your principal – and your previous earnings – are protected by the safety of a “floor.”

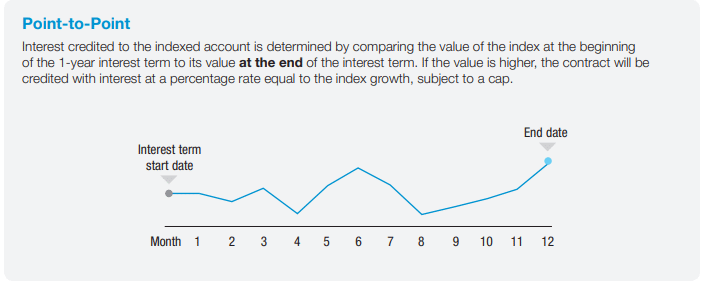

The Symetra Advisory Edge 5 annuity uses a point-to-point tracking for the return that is credited to the account. In this case, the return is determined by comparing the value of the index (or indexes) at the beginning of the one-year interest term to its value at the end of the interest term.

Then, if the value is higher at the end of the term than it was at the beginning, the contract will be credited with interest at a percentage rate that is equal to the growth (but also subject to a maximum, or cap).

The amount of interest credited is subject to a “cap,” though, so if the index(es) performs well, the annuity may not attain the full return of the underlying index. In return for that, however, if the index(es) performs poorly in a given period, your principal – and your previous earnings – are protected by the safety of a “floor.”

The Symetra Advisory Edge 5 annuity uses a point-to-point tracking for the return that is credited to the account. In this case, the return is determined by comparing the value of the index (or indexes) at the beginning of the one-year interest term to its value at the end of the interest term.

Then, if the value is higher at the end of the term than it was at the beginning, the contract will be credited with interest at a percentage rate that is equal to the growth (but also subject to a maximum, or cap).

This, in turn, allows you the opportunity for growth, but with no risk of loss to your principal. Just like with other annuities, the gain that takes place in the account is tax-deferred, so there is no tax due until the time of withdrawal.

When the times comes, you can convert your funds in the annuity to an income stream – with one of your many options being income for life, regardless of how long you may live. This can help to alleviate the concern about running out of income in retirement.

There are a few other features that you get with the Symetra Advisory Edge annuity. These include:

This, in turn, allows you the opportunity for growth, but with no risk of loss to your principal. Just like with other annuities, the gain that takes place in the account is tax-deferred, so there is no tax due until the time of withdrawal.

When the times comes, you can convert your funds in the annuity to an income stream – with one of your many options being income for life, regardless of how long you may live. This can help to alleviate the concern about running out of income in retirement.

There are a few other features that you get with the Symetra Advisory Edge annuity. These include:

- Nursing home and hospitalization waiver(s) – Symetra will waive surrender charges and the market value adjustment (MVA) if you are confined to a nursing home or hospital for at least 30 consecutive days, and for up to 90 days after your release. (Some exceptions may apply here, though.)

- Death benefit – In the event that you pass away, a named beneficiary (or more than one beneficiary) will receive the greater of either the annuity’s contract value (minus any withdrawals and/or charges), or the cash surrender value. By directly transferring the funds to the beneficiary(ies), the funds can avoid probate.

How an Insurance or Financial Advisor Might “Pitch” this Annuity

Over the past several years – especially since the 2008 U.S. recession, and more recently the 2020 COVID-19 pandemic and corresponding stock market correction – safety of principal has been a key concern for many investors. This is particularly the case as they inch their way towards retirement. Unfortunately, though, the more traditional “safe” financial vehicles, such as CDs and regular fixed annuities, can offer safety, but their rates are so painfully low that they can’t even come close to meeting future inflation, much less beating it. But with a fixed indexed annuity like the Symetra Advisory Edge 5 annuity, you are able to alleviate a lot of this worry. That is because this type of annuity offers the opportunity to return higher than a traditional fixed annuity (up to a certain set “cap”), while also keeping principal safe – regardless of what happens in the market. The icing on the cake is the fact that, if the lifetime income option is chosen, the worry about running out of money in retirement has also been taken off the table. Because of this, though, insurance and financial advisors who offer this type of annuity tend to pitch a “best of all worlds” scenario. This, however, can (and does) typically come with some tradeoffs that may not necessarily be all that appealing. One of these is the cap on upward returns. As an example, if an indexed annuity has a cap of 5%, but the underlying index that the annuity is tracking has a stellar year and it returns closer to 10 or even 15%, the return that is credited to the annuity account will be capped at 5%. So, while you do have the opportunity to end up with a higher return than a regular fixed annuity with a set rate of interest, the reality is that the 7 or 8% returns that are touted by some of the annuity marketing websites are not all that likely – especially on an ongoing basis. Also, as with most other fixed indexed annuities, the index that is used is basically a price index, and it will not reflect the dividends that are paid on the underlying stocks in that index. And then there are the fees…Fees Associated with the Symetra Advisory Edge 5 Fixed Indexed Annuity

Even though many fixed indexed annuities don’t hit you with an up-front sales commission – which in turn leaves you less principal to start with – don’t let that lure you into believing that purchasing this annuity will be completely “free.” This is especially true if you need to access your money within the first few years of purchasing the annuity. For instance, while many annuity sales reps will gloss over the “surrender” charges, the reality is that if you access more than 10% of your contract’s value during the surrender period – which in this case is five full years – you’ll pay a withdrawal charge of 2%. On top of that, you can also be required to pay tax on the gain. And, if you make such withdrawals before you have reached the age of 59 ½, the IRS will also require you to pay an additional 10% early withdrawal charge. With all of this in mind, it is essential to treat the purchase of this – or any – annuity as a long-term financial commitment. Otherwise, it could definitely end up costing you!The Annuity Gator’s End Take on the Symetra Advisory Edge 5

Where it works best: After researching all of the ins and outs of the Symetra Advisory Edge 5 annuity, it appears that this particular annuity will usually work the best for those who are looking for:- Safety of principal

- The opportunity for index-linked growth

- Guaranteed lifetime income in retirement

- Need access to most or all of your money within the first several contract years, during the surrender charge period.

- Do not intend to use the lifetime income feature of the annuity.

In Summary

There is a long list of criteria that should be considered when you are thinking about the purchase of an annuity. One of the primary reasons for that is because these products could require that you plunk down a large amount of your overall retirement savings. So, you definitely want to know that you’re making the right choice. In any case, we want to reiterate that an annuity should always be considered as a long-term financial decision – and because of that, it is truly important that you are confident about how the product may or may not fit in with your specific financial goals. When you are considering a fixed indexed annuity, you can be comfortable in that your principal will be safe from market fluctuations, as well as in that you can set it up to provide you with an ongoing retirement income in the future. Given that, you can also attain the security that you won’t run out of income during retirement. In the case of the Symetra Advisory Edge, there can definitely be some great benefits. But that being said, this particular annuity could also fall somewhat short, and quite frankly, there may be some better options that are out there for you – primarily if you are in search of guaranteed lifetime income, along with the opportunity for growth.Do You Have Any Additional Questions on the Symetra Advisory Edge 5 Index Annuity? Did You Find Any Mistakes in this Annuity Review?

We understand that this annuity review went a tad bit long, so we definitely appreciate you sticking with us thus far. However, in this regard, we would much rather that you have “too much” information on this product than to not have enough. So, if you found this annuity review to be beneficial, please feel free to pass it on and to share it with other people who could also find value in it. We also know that, just as with other financial products and services, the information about annuities can change quite frequently. So, if you happened to notice any information in this annuity review that may need to be updated or revised, then please let us know that, too, and we will be happy to make any of the needed updates. Are there any other annuities that you would like us to review? If so, great! Just give us the name of the annuity (or annuities), and our team of highly trained annuity experts will get to it as quickly as we possibly can. Best, The Annuity Gator P.S. If you would like to read more of our Symetra annuity reviews here are some links to check out:- Symetra Custom 7 Fixed Annuity

- Symetra Financial Symetra Edge Plus 7 Fixed Indexed Annuity

- Symetra Single Premium Fixed Deferred Annuity

- Symetra Flexible Premium Fixed Deferred Annuity

- Independent Review of the Symetra True Variable Annuity [April 2018 Update].