It’s no secret that people are living longer these days. Unlike just a few decades ago, today, spending 20 or more years in retirement is becoming more common – and in some cases, people are actually spending more time in retirement than they did in the workforce.

But, while a nice long vacation from work can sound really enticing, the reality is that income must last just as long – and without some kind of ongoing income guarantee, each day that you spend money in retirement can be like watching the gas gauge on your dashboard inching its way towards Empty.

Is that really any way to “relax” during your golden years?

How to Make Your Money Last as Long as You Do

Traditionally, most retirees have been able to count on income from three primary sources. These include:- Pensions

- Social Security, and

- Personal Savings and Investments

Company Pension Plans

First, there are company pensions. Typically, many companies in the past offered their retirees “defined benefit” pension income. As its name implies, this was a set, known amount of income that the retiree could count on each and every month, usually until the day he or she died. In addition, in many instances, some or all of this income would continue for a surviving spouse. Unfortunately, because the employer took on all of the risks in terms of ensuring these ongoing income streams, defined benefit pension plans became much too expensive to continue. So today, it is extremely rare to find organizations that still offer this type of retirement plan. Instead, defined benefit pensions have been replaced with defined contribution plans – the most popular of these being the 401(k). Here, unlike defined benefit plans, a defined contribution plan dictates how much can be contributed each year – but it will not make any type of guarantee as to how much income will be received by the retiree in the future. On top of that, it is the employee – not the employer – who takes on all of the risks. This means if the market has a “correction” and an employee’s retirement plan balance drops in value, it could have a dire effect on his or her future income stream.Social Security Income

Another somewhat wobbly leg of the three-legged retirement income stool is Social Security. When this program was initially enacted, it was meant solely as a safety net to keep retirees out of poverty. But Social Security was never meant to be one’s sole source – or even a primary source – of income in retirement. Today, according to the Social Security Administration, this benefit replaces roughly 40% of an average wage earner’s pre-retirement wages. So, if you are a higher wage earner, it’s likely that this income source will replace a considerably smaller percentage. There’s an even bigger issue with Social Security, though, and that is, due to the vast array of Baby Boomers who have started to retire, there are fewer and fewer workers paying into the system, and more retirees taking out of it. Because Social Security is considered a “pay as you go” system, it is today’s workers who are essentially funding the benefit of today’s retirees. But there may be nothing left for the retirees of tomorrow. Here’s one of the biggest reasons why: Back when Social Security started, there were more than 40 workers paying into the system for each retiree who was receiving benefits. Today, however, the ratio is closer to three workers for every one retiree. And eventually, there may even be more people taking benefits out than there are paying into the system. What do you think will happen to Social Security then? Unless something changes drastically, it won’t likely be a pretty picture.Personal Savings and Investments

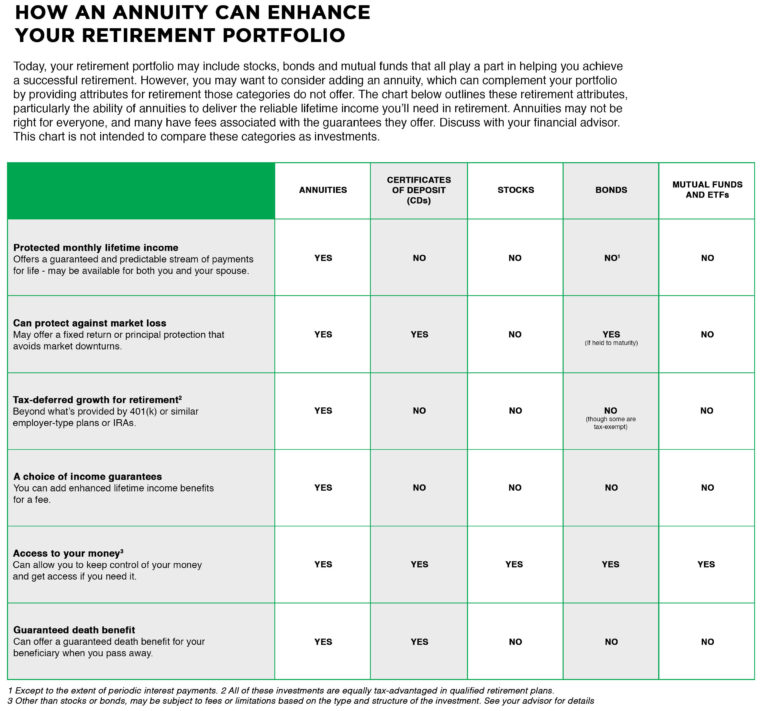

So, this takes us to the third leg of the three-legged retirement income stool – personal savings and investments. Given the issues with the other “legs,” personal savings and investments – which were once considered to be “gravy” for retirees – has begun to play a much more important role in how, and how well, retirees will fare financially. With that in mind, people are seeking ways to turn these assets into an ongoing income stream that will last for the remainder of their lives. And unfortunately, given the incredible volatility of the stock market, taking a chance with your life savings there isn’t the answer. In fact, even at a 2% or 3% annual withdrawal rate, you run the risk of draining your entire portfolio in a matter of just a few short years. But an annuity could help you to turn assets into ongoing income for life.The Benefits of Annuities

Annuities are designed for paying out a regular income stream. Contrary to popular belief, the annuity has actually been around for thousands of years, and a form of these financial vehicles was even used by the ancient Greeks. One of the biggest benefits to having an annuity is that it can provide you with the peace of mind in knowing that regardless of how long you may need it, your income will continue to flow in. But the benefits don’t stop there. In fact, annuities can provide a long list of advantages, both before and after you retire. Let’s break this down by life stage – in other words, the time before you retire, and the time after you’ve said goodbye to your employer. (Note that we’re referring to deferred annuities here for the time before you retire).

Annuity Benefits During Your Working Years

Before we go into detail here, it is important to note that there are several different types of annuities. For instance, with an immediate annuity, you will typically deposit just one, single lump sum (such as money from a 401k, IRA, or another retirement plan), and the income benefits will begin right away (usually within one year). On the other hand, a deferred annuity has a distribution period – when it pays out an income stream – and also an accumulation period. During this accumulation period, you can make one single deposit, or you can make multiple contributions over time. The funds that are inside of an annuity account are allowed to grow on a tax-deferred basis. This means that there is no tax due on the gain, which can allow the money to compound exponentially over time. Depending on the type of annuity you have, there may be different methods of determining the return on your funds. For instance:- Fixed annuities provide a set return over time. And, while this fixed annuity return may be low (similar to that of a CD), your funds are protected from the ups and downs of the stock market.

- Variable annuities provide you with the opportunity to get market-related returns. So, these types of annuities have the ability to provide a much higher return than a fixed annuity. But variable annuities also come with the risk of loss. So, in an up and down market, a variable annuity could put you on edge, as you could lose a substantial portion of your principal.

- Fixed index annuities are a type of fixed annuity that offers a return that is based on the performance of an underlying market index, such as the S&P 500. With a fixed index annuity, a positive return is posted – oftentimes up to a set “cap” – when the underlying index performs well. But, if the index performs poorly during a given year, the annuity will not be dinged with a loss, but rather it is simply credited with a 0% return for that time period. So, while fixed index annuities can provide the ability to earn more than a regular fixed annuity, your principal will also remain protected.

Annuity Benefits After You Retire

When you are ready to begin generating income from an annuity, there are typically several different options that you can choose from. These may include income that is received for a certain number of years. It will also typically include a lifetime income stream. With guaranteed lifetime income from an annuity, you will be able to count on an income stream for as long as you need it. And, if you opt for the joint and survivor income option, both you and a spouse, partner, or another individual can both count on ongoing income for life.Things to Consider Before You Buy an Annuity

Just like with most other things in life, there can be certain tradeoffs to consider when you purchase an annuity. In this case, most annuities will impose a surrender charge if you withdraw more than a small percentage of your account value within the first few years of purchasing the annuity. In addition, if you withdraw funds from an annuity before you turn age 59 ½, you may also incur an additional 10% IRS “early withdrawal” penalty. For that reason, an annuity should always be considered a long-term financial obligation.Still Not Sure If an Annuity Fits into Your Retirement Portfolio?

Annuities tend to have a number of “moving parts,” and for that reason, these products can be somewhat intimidating if you’re not familiar with them. With that in mind, it is always recommended that you gather all of the information you need for understanding annuities before you dive in and commit to one. At Annuity Gator, we make the annuity buying process painless. We offer objective annuity reviews, and we will even help you to compare annuities that you may be considering purchasing. Feel free to reach out to us any time with your annuity questions. We can be reached here.