If you’ve been in the midst of researching retirement income products, then undoubtedly annuities have come across your radar. There are a number of positive features associated with annuities that can make them very attractive products.

But whether or not you should buy an annuity doesn’t depend on the product itself – even if it offers a long list of enticing bells and whistles. Rather, whether or not you should buy an annuity really depends on why you are considering it in the first place.

Is an Annuity Right for You?

Because everyone’s goals and dreams are different, not all financial products can produce the same results. In other words, what may be ideal for someone else, might be far from what you were hoping to achieve. As an example, let’s look at fixed annuities. For some people, a steady rate of return that is set by the insurance company offering the annuity may be the ultimate cat’s meow – particularly if they are seeking the safety of principal. But even though the money in a fixed annuity is safe – regardless of what occurs in the stock market – there are others who would gladly trade all of that safety for the opportunity to earn market-linked returns…even if it also means taking on the added risk of a volatile, or even a downward moving, market.Do Your Financial Goals Align with What an Annuity Can Offer You?

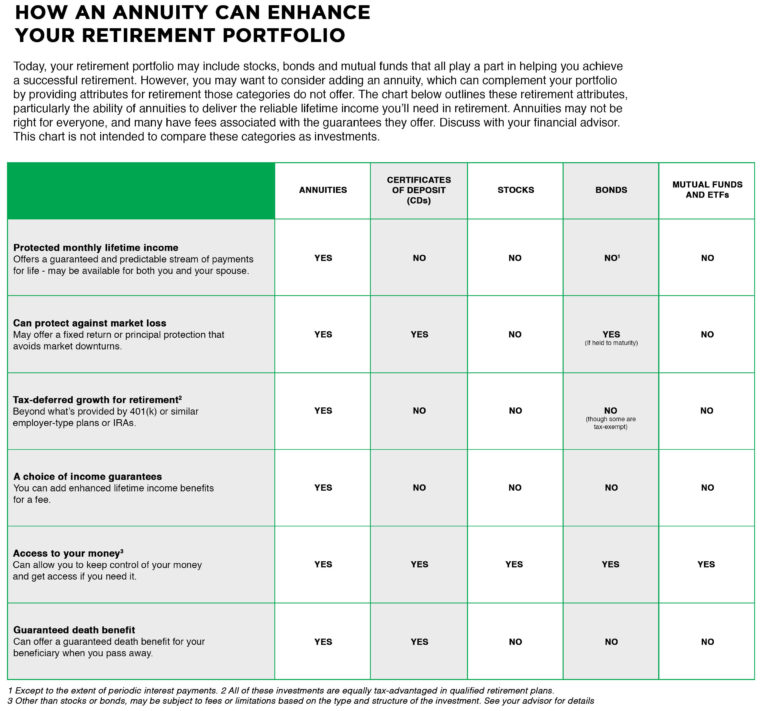

So, what exactly are your financial goals? Are you looking for the chance to earn a nice return quickly? Or instead, are you seeking a slow and steady upward moving account balance, regardless of what occurs in the stock market, or even in the economy overall? When you take a close look at annuities, these products essentially do three things very well. These are:- Adding supplemental lifetime income

- Offering protected principal and/or growth potential

- Protecting funds for a loved one later on (i.e., legacy planning)

Your Personal Purchase Annuity Gauge

In the world of retirement income planning, there is no such thing as a one-size-fits-all strategy or product that is right for everyone. That being said, financial products like annuities should be considered tools to get you closer to your goal, as versus an all-encompassing solution. So, in order to help you determine whether or not an annuity is really right for you, it can be helpful to ask yourself some important questions that pertain to your short- and long-term financial goals, and the best way that you want to go about achieving them. If you still don’t have all of the answers you need regarding whether or not you should purchase an annuity, turning to an unbiased annuity advisor can help. At Annuity Gator, our primary focus is on investigating and comparing annuities. Because of that, we have built up the largest source of annuity reviews online. We also assist consumers one-on-one in determining whether or not an annuity is really right for them – and if so, we walk through comparisons of different annuities in order to narrow down which one might be the best choice for you, given your specific short- and long-term financial objectives. Want more information? Feel free to reach out to us directly at (888) 440-2468, or go through our secure online contact form. We look forward to helping you determine whether or not an annuity is right for you.

P. J. Herold

I am really torn between a regular annuity and a fixed income annuity. My New York Life agent is definitely against fixed index annuities, but I still don’t understand why.

Any help would be appreciated.

Annuity Gator

Hi P.J. Herold– Thank you for your message.

We would be happy to help you understand both types of annuities and compare them side by side to help you see which is better for your situation.

Please feel free to contact us directly, toll-free, at (888) 440-2468 to chat with one of our annuity specialists or visit http://annuitygator.com/contact/

We look forward to hearing from you.

Best. Annuity Gator