What’s Covered in this Athene Annuity Review?

In this Athene annuity review, we’ll cover the following information on the Athene Ascent Fixed Indexed Annuity

- Product Type

- Fees

- Current Rates

- Realistic long term investment expectations

- What to expect, and what not to expect

- Financial ratings of Athene Annuity and Life Company

Annuities can be complex. That’s where having an Annuity Investigator who loves math comes in.

We make the complex, simple.

Annuities are a type of insurance product. The Athene Ascent is a fixed indexed annuity (FIA) that may be appealing to those who are seeking a higher rate of return than that of a regular fixed annuity, but who also want to keep their money safe during the “accumulation”, or savings, phase of the annuity – even during a stock market downturn. In fact, given that the biggest fear on the minds of retirees is losing income and assets while they are still needed, the protection of downside market risk is essential.

At retirement, this annuity can also provide an ongoing income that cannot be outlived if the lifetime option is chosen. Knowing you can count on this ongoing stream of income can allow you to focus on other things in retirement – such as traveling and spending time with family and friends. In fact, annuity income can provide either a nice alternative or supplement to your other retirement cash flow sources.

Fixed indexed annuities can have many pros and cons. There can be both advantages and drawbacks, and because all annuities should be considered long-term endeavors, it is important to have a good understanding as to why this annuity may or may not be a good fit for you.

Otherwise, you could run the risk of getting into a product that sounded good initially, but can be quite expensive to get out of, given its surrender charges during the withdrawal charge period.

A big part of choosing the right annuity – or for that matter, any financial product – is to first determine why you want it, and what exactly you want it to do. Therefore, knowing all of the key details about an annuity can help you to determine whether or not the product is right for you.

The Athene Ascent fixed indexed annuity is primarily designed for those who will need income in ten years or more, and who want to obtain guarantees with growth potential. This annuity offers a unique advantage – particularly if the Income Aspect Income Rider is added, which can offer the power of a 10 percent simple interest crediting rate to the annuity’s income base.

The Ascent annuity actually provides numerous different options in its “suite” of products. These include an array of strong crediting strategies and income payout alternatives. These are all broken down – along with the various income base bonus (where applicable) and other features such as premium bonus (and related vesting schedule).

Annuity and Retirement Income Planning Information That You Can Trust

If you have not been to our website before, we would like to officially welcome you to AnnuityGator.com. We are a team of experienced insurance and financial pros who focus on providing unbiased annuity reviews and other financial details about retirement income. We can provide you with more objective information on annuities that insurance advisors could “overlook” if they are simply trying to make a sale.

So, if you are looking for complete information – and not just the rosy highlights that you’ll typically find in glossy sales brochures – then you have certainly come to the right place. In fact, there could be a number of reasons why you may be here, looking for additional details within our Athene annuity review.

For instance, it is possible that you have recently attended a seminar or online webinar, where in return for a free lunch or steak dinner, the presenter invited you to schedule an appointment and now you’re being pitched this product.

But, while the opportunity to take part in market gains, while keeping your principal safe – along with a guaranteed lifetime income in retirement – may have sounded appealing, you may not have heard the entire story.

If you’ve been searching for this fixed indexed annuity’s pros and cons on other websites, you may have been lured in by some bold claims, such as:

- Highest income payouts

- Market Index-Linked Growth

- Lowest fees

- Quick annuity quotes

- Top-rated carriers

Sound familiar?

While these websites and financial salespeople tout on about the glory of annuities and other positive product details, what they often won’t tell you is that there can be some pitfalls to look out for.

Just to be clear here, we are fans of annuities (when used properly and in the precise amounts) – but we also believe that consumers need to hear not just the good, but also the bad and the ugly, in order to make a well-informed decision. This is particularly important as the purchase of an annuity could very well require most or all of your hard-earned retirement savings.

What you will find here at AnnuityGator.com is that we are the original online source of providing unbiased annuity reviews. We have been at this for quite some time now – far longer than most of the other annuity websites.

Yet, because we have built a name for ourselves in the annuity industry, there has been a spark of “copycat” websites that try to do what we do.

Based on our experience, we’ve actually discovered that none of the benefits of an annuity really matter until you first understand what your primary reason is for buying it.

In addition, even if you are seeking a nice rate of return, most fixed index annuities will not be able to produce 7 to 8% – and definitely not consistently over time.

Want to find out how annuities really work – and how they may, or may not, work for you? Then feel free to instantly download our

So, if you’re ready to learn more about the Athene Ascent fixed indexed annuity pros and cons – and why it may or may not work for you – then let’s dive in.

Athene Ascent Fixed Indexed Annuity at a Glance:

| Product Name | Ascent Annuity |

|---|---|

| Issuer | Fixed Indexed Annuity |

| Type of Product | Athene Annuity and Life Company |

| Standard & Poor's Rating | A (as of April 2021) |

| Phone Number | (888) 266-8489 |

| Website | https://www.athene.com |

Opening Thoughts on the Athene Ascent Fixed Indexed Annuity

Athene Annuity and Life actually got its start in 2009, when the financial crisis and resulting capital demands caused many financial and insurance companies to exit the industry. Athene has been able to fill this “void” with its strong and stable capitalization, as well as an experienced management team.

If you’ve heard the name Athene online or during a seminar about annuities, it could be that it’s because this is one of the fastest-growing fixed index annuity companies in the industry right now. With Athene’s experienced management team, the company has grown from a start-up just a decade ago, to a firm that holds nearly $133 billion in total GAAP assets, more than $113 billion in invested assets, and more than $10 billion in total equity.

So financially, Athene is strong and stable. In addition to it’s a rating from S&P, the company has also earned an A from A.M. Best and an A from Fitch. The company also holds approximately $1 billion in excess capital.

Over the past several years, fixed indexed annuities (FIAs) have become more popular – predominantly as a way of obtaining a nice potential return, as well as the safety of principal. Due in large part to the continued volatility of the market, fixed indexed annuities have led many investors to believe that they are keeping their money safe, while also building up a nice retirement income stream for the future.

Some annuity sales agents use the term “hybrid,” when they are referring to this annuity because it has multiple annuity features rolled into a single product.

But in reality, “Hybrid Annuity” is just a marketing term. It’s nothing special, and in reality, annuities (for the most part) have always been hybrid in nature because they do more than just one thing. (They can grow money and pay out income).

The Athene Ascent annuity suite provides several different options for investors, based on specific goals and time frame. Overall, though, the Ascent products offer the following features:

- Guarantees – Because of the product’s fixed interest crediting strategy, annuity owners can be assured that their money will get a minimum return. The rate of interest is set each year by the company and is in turn guaranteed for that next contract year.

- Opportunity for Growth – Based on the performance of an underlying index, there is also the opportunity for growth, especially in good index years.

- Protection of Principal – Because there is no downside risk, the principal is protected in the Ascent annuity – and, with no loss of principal, future gains can continue to build and compound.

- Income – There are several income options available on the Athene Ascent annuity – including a lifetime option. If the lifetime income option is chosen, income will continue throughout the remainder of the annuitant’s lifetime, regardless of how long that may be. Having a stated amount of incoming cash flow could help you with meeting your future retirement income goals.

Because people today are living longer than ever before in history, running out of income in retirement is a key concern for many. In order to help in combating this fear, many fixed indexed annuities include riders that can provide income that cannot be outlived.

In the case of the Athene Ascent, the income base is equal to the premium, plus any applicable income base bonus. The income base on this product will be credited with a simple interest credit. Then, on the contract anniversary, the interest credit will be calculated based on the premium minus withdrawals, multiplied by an income base guaranteed simple interest rate.

There are also additional perks on this annuity, such as the ability to obtain an enhanced income benefit if the annuitant has been confined to a qualified nursing home for 180 out of the last 250 days.

While all of these benefits may sound enticing, though, it can still be difficult to know for sure which – if any – annuity will be right for you (and how much money to place into them). So, if you still have questions or concerns, and you want some first-hand and unbiased information, please feel free to reach out to us directly via our secure contact form here.

Before we get into the gritty details, here are some legal disclosures…

This is an independent product review, not a recommendation to buy or sell an annuity. Athene USA has not endorsed this review in any way nor do we receive any compensation for this review. This Athene annuity review is meant to be an independent review at the request of readers so they could see our perspective when breaking down the Athene Ascent fixed indexed annuity pros and cons. Before purchasing any investment product be sure to do your own due diligence and consult a properly licensed professional should you have specific questions as they relate to your individual circumstances. All names, marks, and materials used for this review are the property of their respective owners.

For additional information on how to compare fixed indexed annuities so that you can decide which may be the best one for you, in order to obtain our free annuity buyer’s guide.

How Athene Describes The Ascent Fixed Indexed Annuity.

In the age of the one-size-fits-everything movement, it’s refreshing to see a company dedicated to a specific focus: innovative financial products designed to protect and create income. And that’s it! They’re not trying to give you double-digit returns, sell you mutual funds, stocks or bonds.

They are kind of like the burger joint that sells high-quality all-beef patties with hand cut French fries for a fair price and that’s it. They don’t roast chicken, toss pizzas, or hand weave baskets.

They are kind of like the burger joint that sells high-quality all-beef patties with hand cut French fries for a fair price and that’s it. They don’t roast chicken, toss pizzas, or hand weave baskets.

Athene sells three kinds of annuities all designed to turn your retirement savings into a lifetime income stream, so if you’re looking for income, this is an insurance company that specializes.

It is the claims-paying strength of the insurance company that backs your annuity, so if you’re retiring without a pension, you want to make sure the company who holds your source of income is strong.

That being said, the company has earned decent ratings from the insurance company rating agencies, including a(n):

- A from S&P

- A from Fitch

- A from A.M. Best

So, they have good “report card.”

Unfortunately, though, the company has had some issues with consumer complaints over the years – including 136 complaints filed through the Better Business Bureau. This may have been a catalyst in the company having a C- rating from the BBB. In fact, as of June 2019, more than 100 of these complaints centered around having a problem with the company’s product or service.

You can check out the Athene annuities complaint summary HERE.

Athene describes the benefits and features of the Ascent annuity as having guarantees, growth potential, protection, and the ability to obtain tax-deferral of the funds inside of the account. The Ascent annuity also offers the option of a death benefit, so that you can guarantee your loved ones a source of funds if income is not taken from the annuity. You’ll find additional information by checking out the Athene Ascent brochure.

The way an annuity guarantees lifetime income is through the purchase of an income rider. But here’s the thing: the benefits and features offered by riders vary from insurance company to insurance company, even if the annuity is called the same thing! For instance, the riders for variable annuities will often time have wildly different guarantees.

The cool thing about this particular income rider is that it doesn’t just guarantee your income for five or 10 or even 20 years – but rather it guarantees the income for life, whether you live to age 85 or 105. There are, of course, some exceptions.

As far as an annuity, Athene gives you some pretty generous terms as far as having access to your money. For instance, it allows you to have free withdrawals – up to 10 percent of your annuity’s accumulated value. It can also double your income in the event of a qualified long-term care situation.

But you can’t simply take out as much as you want and still expect to get the lifetime income guarantee. If you take out more than what they call the “Lifetime Income Withdrawal” amount, you could run into problems. And if you cash in your annuity or make too large of a withdrawal before the contracted surrender period, you will incur a withdrawal charge and a market value adjustment will be applied.

Here are the basic rules in a nutshell:

When you elect an income rider, the insurance company invests the money you put into the contract and it creates a separate account. This separate account grows at a different rate than your regular account. Athene calls this special account the Income Base and the regular account the Accumulated Value.

Now, here is where things can get a little confusing, and financial salespeople who sell FIAs may not take the time to explain to consumers exactly what they are getting into when they buy an FIA. Here is what you need to know:

The Accumulated Value is the actual value of your annuity policy

- When you make a withdrawal, the money is deducted from this account.

- When you receive an income payment, the money is deducted from this account.

- If you have purchased income rider guarantees, and this account value falls to ZERO, then – guess what?!? – you still get the income payments for the rest of your life (unless you took out an Excessive Lifetime Income Withdrawal – we’ll talk about that next).

The Income Base is the value of the account created by the purchase of the income rider.

- This account is the one that grows using special Income Base rider options. The Income Base (as defined by Athene) is made up of three things:

-

- 1. The initial premium you put in plus any bonus money

- 2. The simple interest credits

- 3. The indexed interest credits should you chose the indexing method.

- These three elements combined are what allow the Income Base account to grow at a more accelerated rate than the regular Accumulation Value of the actual contract.

- This account is what is used to CALCULATE the amount of your lifetime income.

- The amount of your lifetime income is calculated using a simple math formula:

Your Income Base X Your Lifetime Income Withdrawal % = Your Income

Quick aside here – this formula makes one thing very transparent: that withdrawal percentage is a very important number. It is the percentage that really tells you more about how much income you will actually get than many of the other numbers used when people try to sell you this and other FIA-type products.

If you want to test how much income this annuity will give you versus another annuity for the same dollar investment, please feel free to reach out to us so that we can assist you in calculating the income accurately.

Moving onward:

- The money in the Income Base account is NOT money that you can take out as a lump sum to go buy a new condo with.

- The money in the Income Base account does not have a cash value or a surrender value – meaning, should you cash out the annuity before taking income, this money doesn’t exist.

- If you elected the death benefit rider instead of the income rider, then your beneficiaries will receive the higher of the two accounts – either the Income Base or the Account Value – whichever is greatest. (Nice, huh?)

- If you take out MORE than the income amount specified by the simple math formula, then Athene considers this an Excessive Lifetime Income Withdrawal.

- If an Excessive Lifetime Income Withdrawal reduces your actual account (the Accumulated Value account) to ZERO, then – guess what?!? – your guaranteed income payments STOP.

This makes sense when you think about it from the insurance company’s point of view, but what might that look like to you?

Imagine you have an FIA, and you have it set up so that in ten years’ time, you’ll start receiving a check for $2,200 every month. You don’t have to worry about the stock market, about running out of money, or about what will happen to your spouse, because you elected the rider guarantees. You are all set.

Now, let’s say your daughter goes through a terrible divorce and she needs to borrow some money for a down payment on a new house in a safe neighborhood for the grandkids. If you dip into your annuity to lend her this money, and you take out an Excessive Lifetime Income Withdrawal, then your lifetime income guarantee benefit could be canceled or, at the very least, reduced. Ouch!

These are just some things you want to be aware of before you buy into any annuity. You want to understand what it was designed to do, and how it does that. Any benefit you get is going to come with a counterweight compromise, so you have to understand what that compromise is so you can adjust your retirement strategy accordingly.

How Financial Advisors Might Pitch This Annuity to You

Given its opportunity for growth, yet also the protection of principal, a financial or insurance sales agent may pitch the Athene Ascent fixed indexed annuity as a vehicle that can provide you with a “best of all worlds” scenario. This, however, is not necessarily true.

With that in mind, let’s break down Athene Ascent’s fixed index annuity pros and cons. When financial salespeople talk about the performance of an FIA, what they are usually talking about is the enhanced growth rate you get with the purchase of an income rider.

There is a fee for this rider, and the charge is deducted monthly from both the Income Base account and the Accumulated Value account (which is the actual value of the contract.)

In exchange for this fee, you’ll be getting a guaranteed income base that grows every year until you decide to turn on your lifetime income, and that’s what FIAs are famous for. Now, let’s consider realistically what kind of growth you can expect from the Athene Ascent.

Athene basically gives you two ways to grow the money you want to protect for retirement income.

What’s wonderful about both these options is that it gives an investor at or near the time of retirement a place to put a portion of their savings where it will be protected from market loss while still earning a pretty decent return.

Option 1 – Fixed Strategy: you can choose a “Simple Interest Rate” where your money grows at the same rate every year no matter what the market is doing. The Income Base guaranteed Simple Interest rate (as opposed to compound rate) is currently 10% for the first 10 years. After that, you’ll get a 5% simple interest credit for up to 20 more years guaranteed for contracts issued with a premium of $50,000 and above.

Every annuity out there worth its salt offers these enhanced growth rates with the purchase of an income rider, but a lot of them end once you start taking the income. When you consider that the average rate of inflation is 3.22% annually, then you might start to see the value of this deal. Just remember, the only way you can spend this money is by taking the income because it’s growing in that special account.

While the Athene annuity rate sheet may or may not be accessible online, you can find the most updated fixed rates for the Athene Ascent fixed index annuity by talking with an annuity specialist.

With that in mind, feel free to reach out to us regarding Athene annuity rates – or any other questions that you may have regarding annuities – via our toll-free number at (888) 440-2468.

Or, you can contact us through our secure online contact form to ask your annuity question using our secure contact form.

Option 2 – Indexed Strategy: you can choose the guaranteed growth PLUS Interest Credits. This option gives you a lower guaranteed “Simple Interest Rate” in exchange for Interest Credits linked to a market index. These credits are applied to the Income Base and you are guaranteed never to earn less than 0%. According to the hypothetical charts and graphs presented in the Athene brochures, this method has the potential to earn – eh, roughly speaking – about 13% higher or lower than the guaranteed Simple Interest Rate.

Does this annuity really earn better returns than other annuities? If not, are there others potential alternatives that you should take a look at?

FIAs offer limited growth, which means you don’t get to capture the full glory of a market gain. You trade that in exchange for more secure protection. The Athene uses Annual Cap Rates and Participation Rates which basically give you some, but not all, of the good times.

For example, IF your annuity has a 13% cap, your Income Base would only grow at 13% when the index earns returns of 13% or higher. If the index earned 3%, you would get a 3% gain. If the index earned 23%, you would only get 13% of the gains. If the index drops by 23%, your account would still grow according to the guaranteed minimum interest amount, and it would not lose any money due to market loss.

What about the free bonus money? You might hear about bonus money anywhere from 1 to 3% of your initial payment, credited to your account as a gift at the time you sign up for this annuity. It is sometimes the case with other FIAs that the bonus money is only applied to the Income Base and not the actual Account Value.

With the Athene, the bonus is credited to BOTH accounts. Remember the magic formula?

Your Income = the Income Base X your Lifetime Income Withdrawal %

The more money you have in your income base, the higher the potential income amount.

But does the Athene really give you more income than other annuities?

Great question – we’re glad you asked. Some investors may get tricked by talk of high returns. All the focus these days seems to be on the rate of return, but at the end of the day when all the smoke and mirrors are rolled off the stage, what really what matters most is the amount of INCOME you will get from your money.

The bottom line here is that Athene strives to be an industry leader in the annuity arena – and in many ways, it is. However, recently the company has reduced some of their guarantees. And, since the recent rate change on this product, there are some other fixed indexed annuity providers that may outperform the Ascent annuity. Click here to see which annuity has the highest guarantees in your state.

What About the Fees?

Not unlike other annuities, the Ascent has several areas where you will find charges and fees. For instance, there is an income rider charge, which is deducted from the annuity’s accumulated value and the income base. Unfortunately, you really can’t avoid this fee, if you are seeking guaranteed lifetime income with this annuity.

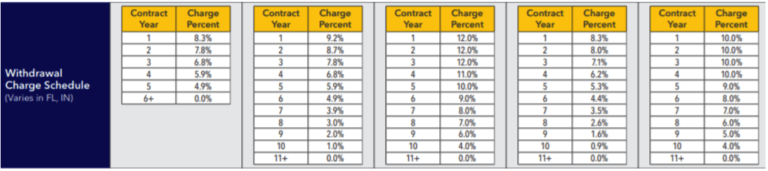

There is also a fairly hefty withdrawal charge. Other than with the Ascent 5 – which has six years of surrender fees – the Ascent 10, Ascent 10 Bonus, Ascent 10 Bonus Select, and the Ascent Bonus Pro will lock you in for 11 years before you are fully “vested”. So, be sure that you’re familiar with the withdrawal fee schedules if you opt to go with any annuity.

The Annuity Gators End-Take on the Athene Ascent Fixed Indexed Annuity Pros and Cons

Where it works best:

The bottom line on the Athene Ascent FIA is that this annuity may work the best for people who are looking for the following features:

- Safety of principal in any type of stock market environment – including a significant market downturn

- The opportunity for index-linked growth

- Guaranteed lifetime income in retirement

Where it works the worst:

The Athene Ascent Fixed Indexed Annuity may not be such an ideal fit for you if you are looking for:

- Access to most or all of your money within the first eleven years

- You do not intend to use the lifetime income feature of the annuity

In order to truly get an idea of whether or not a fixed indexed annuity such as the Athene Ascent annuity is right for you,

You can also benefit by running the numbers on the Athene Ascent fixed index annuity calculator. While many annuity sales brochures will provide you with hypothetical information, running the figures based on your specific situation will at least get you somewhat closer to being in the ballpark. Click here if you would like us to run an individual spreadsheet for you.

In Summary

There are many key factors that you need to consider when you are deciding whether or not an annuity is right for you. But, regardless of the type of annuity, you are thinking about, as well as where you may purchase it from, all annuities should be considered as long-term endeavors.

In the case of the Ascent annuity, you can certainly be assured that your principal is protected – even in a market that is moving downward. You will also have the opportunity for a higher return than that of a regular fixed annuity. And, when you are ready to convert your funds over into an income stream, you can count on a guaranteed lifetime cash flow, provided you choose the lifetime option.

But, even though there are some nice features about the Athene Ascent fixed indexed annuity, this particular product may still fall short – and quite frankly, there may be some better options out there for you.

So, if you still have any questions or concerns that have not been answered in this review, or if you would like to talk directly to an unbiased annuity expert, then please feel free to reach out to us via our secure contact form below:

[gravityform id=”15″ title=”false” description=”false”]

Need Any Additional Information About the Athene Ascent Fixed Indexed Annuity? See Any Mistakes In This Athene Annuity Review That Need Correcting?

We realize that this Athene annuity review ran somewhat long – and for that, we do appreciate you sticking with us to the end. Our thought, though, is that we would much rather provide you with “too much” detail regarding this fixed index annuity’s pros and cons, as versus not enough. So, if you happened to find this Athene annuity review helpful, please forward it on to anyone else who you feel might also benefit from the information. You can also request product information on other annuities, too, by contacting us.

We also understand just how quickly information about annuities can change – so, if you found any place in this review where the details need to be updated, please also let us know and we will hop on those updates right away.

Are there any other annuities that you would like to have reviewed?

We’re on it. If you would like additional information in the form of an annuity review that is not already on our website, then just let us know the name of the annuity or annuities, and our team of annuity geeks will get to work on them.

Best,

The Annuity Gator

P.S. We included a few more related links to the Athene Ascent Fixed Indexed Annuity below that you might find useful:

- Athene Ascent Complaints

- Athene Ascent Income Rider

- Athene Ascent Statement of Understanding

- Athene Ascent Enhanced Income Benefit Doubler

- Athene Ascent Death Benefit (Continuation Options)

P.P.S If you would like to read more of our Athene Annuity reviews here’s some links to check out:

- Athene Balanced Choice Annuity (BCA) Elevate Fixed Indexed Annuity

- Athene Ascent Fixed Indexed Annuity

- Athene Income Select Bonus Fixed Index Annuity

23 Comments

Thanks for sharing this detailed review of the Athene Ascent Fixed Indexed Annuity. I’m currently considering purchasing an annuity to provide a steady income stream in retirement, and this review has provided valuable insights into the pros and cons of this particular product. I appreciate the thorough analysis of the features and benefits, as well as the potential risks and drawbacks. It’s helpful to have this information to consider as I make my decision. Keep up the great work!

I have an Athene BAC account for 2 years I want to start taking out the 10% that is allowed without fees.

Do I need to be aware of any other hidden fees? I do have a death rider. I am moving money over to another Jackson account to diversify.

Hi Karen– Thank you for your message.

We would be happy to support you with this. Rather than sending information back and forth via email, ee would love to speak with you and answer any questions you might have. Please feel free to contact us directly, toll-free, at (888) 440-2468 to chat with one of our annuity specialists or visit https://www.annuitygator.com/contact/

We look forward to hearing from you.

Best,

Annuity Gator

I just signed up to purchase FIA 3 days ago, is there a 3 day remorse withdrawal

Hi Jon – Thank you for your comment. Yes, annuities have a “free look” period. During this time, you can receive your deposit back, without having to pay surrender charge penalties. Depending on your state, this free look period could be anywhere from 10 to 30 days. Please let us know if we can help further by contacting us directly, toll-free, at (888) 440-2468, or via our secure online contact form at https://www.annuitygator.com/contact/. Best! The Annuity Gator

You really need to do an update on this particular annuity as there are numerous complaints against this company on the BBB website. Athene sold their services and have had outstanding issues. 135 complaints in the last 3 years and only 68 have been resolved in the past 12 months. That sounds like a pretty terrible record to me.

Hi Pat – Thank you for your comment and for letting us know about the updated that is needed on that annuity. (Things change quickly in the market, and as our annuity database grows, we may not get to the updates as quickly unless we are notified). We are currently working on the updated review now for the Athene Ascent FIA, so please check back soon to take a look. Best. – Annuity Gator Team

Hi, Great blog. We are considering a two Athene Fixed Index Annuity: Athene Ascent Accumulator 10 Annuity and Performance Elite Plus 15 Annuity. They both operate on the BNP Paribas Multi Asset Diversified 5 Index. They appear to have a good historical record for returns. Have you heard of these two annuities or their index? Would appreciate your thoughts? Thanks

Hi Steven – Thank you for your message. Either could be a viable alternative, depending on what you are looking specifically for the annuity to do. We would be happy to help you in determining which may be the better option for you, but we would first need to get some additional information in order to provide you with the best route for you. Rather than sending sensitive personal details back and forth via email, please contact us by phone at (888) 440-2468. We look forward to speaking with you. Best. – Annuity Gator Team

Hi, Great blog. We are considering two Athene Fixed Index Annuities: Athene Ascent Accumulator 10 Annuity and Performance Elite Plus 15 Annuity. They both operate on the BNP Paribas Multi Asset Diversified 5 Index. They appear to have a good historical record for returns. Have you heard of these two annuities or their index? Would appreciate your thoughts? Thanks

Hi Steven – Thank you for your message. Yes, we have checked out these annuities, and they do have a good track record. As far as them being a good fit for your specific portfolio, though, we would need to obtain just a bit more information from you, so that we can determine whether or not one or both would work well given your goals, time frame, etc. Rather than emailing sensitive personal information back and forth, though, it would be best to discuss by phone. Please contact us directly, at your convenience, at (888) 440-2468. Thanks. We look forward to hearing from you. Best. – Annuity Gator Team

Hi Steven, did you ended up purchasing the two annuities ? If you did, do you mind sharing with your thoughts or findings ? I am now at 55 and thinking of purchase FIA and was looking at Allianz 222 but my friend has told me about Athene

Thanks

Steve

Hi Steve,

Before making any financial decision, we ask that you consult with an expert. Here at Annuity Gator, we can help with that, and look at all the in’s and out’s to help you make the best decision depending on YOUR financial goals.

Please feel free to contact us directly, toll-free, at (888) 440-2468 to chat with one of our annuity specialists or visit http://www.annuitygator.com/contact/

We look forward to hearing from you.

Best.

Annuity Gator

Very good information regarding this annuity that I’m thinking of buying. Can I call you before I proceed?

Hi Norma – Thank you for your message. Yes, please feel free to contact us directly, and we can help to answer your questions and provide you with any additional information that you may need. Our direct toll-free number is (888) 440-2468. We look forward to speaking with you. Best. – Annuity Gator Team

Hi Norma – Thank you for your message. We would be happy to go over more information with you via phone. We can be reached toll-free at (888) 440-2468. Thanks, we look forward to hearing from you. Best. -Annuity Gator Team

Hi Norma – Thank you for your message. We would be happy to help with any additional questions that you may have. We can be reached via phone, toll-free, at (888) 440-2468, as well as by email by going to http://www.annuitygator.com/contact/. We look forward to hearing from you. Best! The Annuity Gator

I have recently been presented with a proposal to purchase Athene BCA Elevate, a single premium fixed indexed deferred annuity. I know nothing about annuities. Would you comment about this particular investment?

With thanks,

Susan

Hi Susan – Thank you for your message. We would be happy to provide you with any additional information, as well as to walk through some scenarios with you in terms of the BCA Elevate and how it may (or may not) work in your specific situation. In order to do so, though, we would need to get some information from you. Rather than sending sensitive details back and forth via email, please feel free to contact us directly via phone at (888) 440-2468. We look forward to talking with you. Best. – Annuity Gator Team

Hi Susan – Absolutely! In fact, we can “test” this (or any) annuity, based on your specific situation (i.e., contribution, time frame, etc). In order to do that, we would need some additional information from you. This would best be done via phone, rather than passing sensitive details back and forth in emails. Please feel free to contact us directly, toll-free, at (888) 440-2468, or you can set up a specific time to chat with us by going to http://www.annuitygator.com/contact/. We look forward to hearing from you. Best! The Annuity Gator

Very informative, simple and clear that newly retired investor can understand. Thank you very much for the objective reviews.

My financial advisor sold me:

1) Athene ascent10 bonus2.0 and

2) Nationwide new heights 12 fixed indexed annuity.

Are these good products? Please advise.

Thank you!

Hi Isabelita – Thank you for your comment. These are very good products – depending on your specific financial goals. If you contact us directly at (888) 440-2468, we can provide you with more detailed information. Best. -AnnuityGator Team

Hi Isabelita – Thank you for your message. We would be happy to discuss some potential options with you. In order to provide you with the best advice, we would need to get a bit more information from you. Rather than emailing sensitive details back and forth, though, it would be best to chat via phone. Please feel free to reach out to us directly, toll-free, at (888) 440-2468. We look forward to speaking with you. Best. -AnnuityGator Team