What Will Be Covered in this Review?

In this review, we will be discussing the following information regarding the CUNA Mutual MEMBERS Future Income Annuity:- Product type

- Fees

- Current rates

- Realistic long-term return expectations

- How it is used

- How it is most poorly used

Annuities can be complex. That’s where having an Annuity Investigator who loves math comes in. We make the complex, simple.

If you’ve been trying to decide whether or not to purchase an annuity because you want to ensure that you won’t run out of money in the future, there are a lot of good options out there for you – including the CUNA Mutual MEMBERS Future Income Annuity. This annuity can offer you a lifetime income, no matter what happens in the market, so it can alleviate the worry about dwindling cash flow. This is especially the case if you anticipate that you will live a long life span. Deferred income annuities, or DIAs – which are also often referred to as longevity annuities – are a type of annuity product where you contribute a lump sum of money with an insurance carrier, in exchange for a guaranteed lifetime income stream that begins at a future date…in some cases, not for 30 or even 40 years. Because of that, DIAs can sometimes be used as a pension of sorts for those who don’t have a defined benefit pension plan through an employer, or those who may lose other pension income due to the loss of a spouse. However, while this lifetime income stream may sound ideal, before you run out and purchase the MEMBERS Future Income Annuity from CUNA Mutual – or any annuity, for that matter – it is important that you first have a good understanding of how the product works, and how it may (or may not) work well for you. Over the past decade or so, annuities have become much more popular, primarily as a method of generating an ongoing income stream for those who are in retirement. Yet, due in large part to this increased demand, there are many insurance carriers that have introduced more products out into the market place, and unfortunately, this can make what is already a confusing product even more so! With that in mind, unless the insurance or financial advisor you currently work with specializes in annuities, then it is recommended that you conduct some additional research on these products, as they will usually require you to commit a large amount of your savings to them. This is where we can help.Annuity and Retirement Income Planning Advice that You Can Trust

If this is the first time you have visited our website, please allows us to begin by officially welcoming you here to Annuity Gator. Who exactly are we? Annuity Gator is comprised of a team of experienced financial experts who are dedicated to helping you decode the complicated world of annuities. Here, we strive to create unbiased, yet highly comprehensive, annuity reviews – and we have been at this for far longer than most of those “copycat” websites out there. Annuities are a unique product in that they are the only financial vehicle that can make the promise of providing you with a lasting, lifetime income stream. Unfortunately, though, some insurance and financial advisors who work out in the field – oftentimes unintentionally – tend to make these financial vehicles sound better than they actually are. Working with an advisor who isn’t quite sure how products work can be dangerous to your financial health. This can be particularly true when it comes to annuities because once you commit to purchasing an annuity, you could face some pretty stiff penalties if you want to take all your money out soon afterward (or even over the next several years) due to surrender fees. Many annuity sales reps and even many of the annuity websites that you’ll see online will make some pretty bold claims about the performance of the annuities that they offer, such as:- 7 to 8% return

- Low fees

- Guaranteed income for life

- No market risk

CUNA Mutual MEMBERS Future Income Annuity at a Glance

| Product Name | MEMBERS Future Income Annuity |

|---|---|

| Issuer | CUNA Mutual |

| Type of Product | Deferred Income Annuity |

| S&P Rating | A |

| Phone Number | (800) 356-2644 |

| Website | https://www.cunamutual.com/ |

Opening Thoughts on the CUNA Mutual MEMBERS Future Income Annuity

Founded more than 80 years ago by credit union leaders who were looking for an insurance and investment partner they could trust, CUNA Mutual offers a wide array of financial products to help its customer grow and protect wealth. In fact, CUNA Mutual describes itself as being “A financial services company serving financial institutions and their clients worldwide”. As of year-end 2017, the company has over $20.5 billion in assets and had taken in roughly $3.5 billion in total revenue. Due in large part to its financial strength and stability, CUNA Mutual is rated highly by the insurance company rating agencies with an A from A.M. Best, an A2 from Moody’s Investors Service, and an A from S&P Global. With a deferred income annuity or DIA, the volatility of the stock market does not affect the amount of income that you’ll receive in the future. When you purchase a DIA, you decide when you wish to start receiving your income, and the insurance company will then guarantee you a set income that will start at your chosen date in the future. Many deferred income annuities will also let you make subsequent contributions into the contract. However, the way that these are factored into your future income can vary from one DIA to another. It can also be dependent on the frequency of such subsequent contributions into the annuity.Before we get into the in-depth details, we have some legal disclosures to present…

This is an independent annuity product review. It is not a recommendation to purchase or to sell an annuity. CUNA Mutual has not endorsed this review in any way, nor do we receive any type of compensation for providing this review. This annuity review is meant solely to be an independent review at the request of our readers so that they may see our perspective when breaking down the positives and the negatives of this particular annuity. Prior to committing to the purchase of any type of insurance and/or investment vehicle, it is critical that you do your own due diligence, and that you also talk with a properly licensed professional if you have any questions that relate to your specific situation. All of the names, materials, and marks that have been used in compiling this annuity review are the property of their respective owners. For more details on how to compare fixed annuities so that you can decide which may be the best one for you, click here in order to obtain our free annuity report.How CUNA Mutual Describes the MEMBERS Future Income Annuity

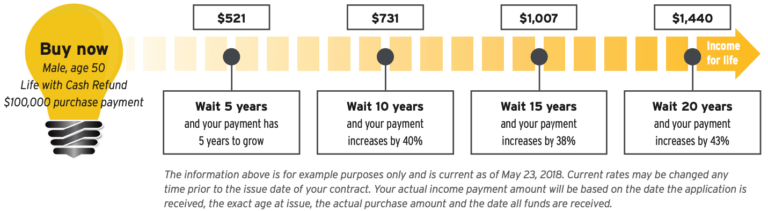

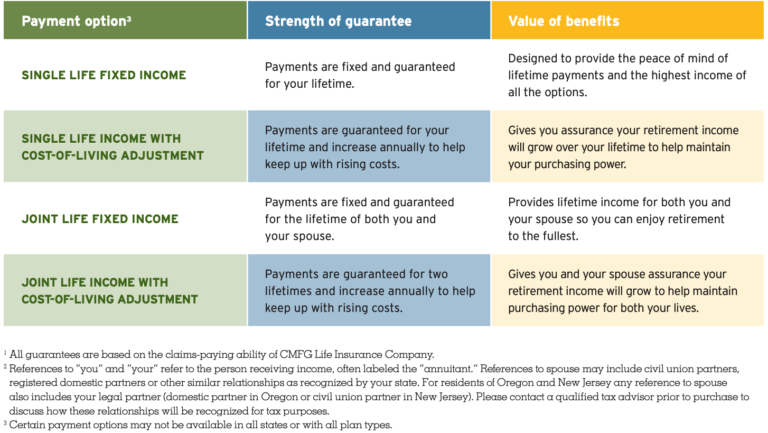

CUNA Mutual describes the MEMBERS Future Income Annuity as an insurance contract that protects your retirement income and guarantees that it will be there as long as you need it. With this annuity, you can receive lifetime income without the worry of market risk. In fact, regardless of what happens to stocks and bonds, your income from this annuity will be secure. The Future Income Annuity offers a wide range of options so that you can basically customize your income payments. This type of annuity is often referred to as a personal pension. That’s because, similar to a defined benefit pension, a DIA guarantees a future stream of income. And in this case, the longer you wait to start receiving your guaranteed income, the higher your monthly payments will be. There are several different ways that you can opt to receive your income, too. For instance, you can choose to receive income for just yourself – either with or without a cost of living adjustment going forward – or you can opt to have the payments continue throughout the lifetime of both you and your spouse.

There are several different ways that you can opt to receive your income, too. For instance, you can choose to receive income for just yourself – either with or without a cost of living adjustment going forward – or you can opt to have the payments continue throughout the lifetime of both you and your spouse.

For more in-depth details regarding the CUNA Mutual MEMBERS Future Income Annuity, you can check out the product brochure HERE.

For more in-depth details regarding the CUNA Mutual MEMBERS Future Income Annuity, you can check out the product brochure HERE.

How an Insurance or a Financial Advisor Might “Pitch” this Annuity

When it comes to our money, it’s nice to have guarantees. The MEMBERS Future Income Annuity from CUNA Mutual can offer you some nice income-related guarantees, which can in turn, allow you to sleep better at night, knowing that you won’t run out of income in your lifetime. Because of these guarantees, it is likely that an insurance or financial advisor who is discussing this annuity with you will key in on the guaranteed income feature. In addition, DIAs will oftentimes offer higher income payments that regular immediate annuities. This is because of your age when you start such payouts is typically older than it would be if you take income from a regular deferred and/or immediate annuity. Therefore, this too is a feature that an advisor might focus on when discussing this – or any – DIA annuity with you. However, prior to moving forward and making a long-term commitment to purchase this annuity, there are a few items that you should know, which may or may not deem this to be the best product for you. For instance, when you purchase a DIA, you will typically need to forfeit your principal in exchange for the future income stream you’ll receive. It is also important to note that deferred income annuities are not liquid financial vehicles. When you invest in this type of annuity, you will usually completely forfeit the initial premium. In addition to that, because it could be many years before you start to take your income stream, it is possible that you may not live long enough to collect on the income stream. With that in mind, you really need to determine whether or not you want to take this big of a chance with your retirement savings.The Annuity Gator’s End Take on the CUNA Mutual MEMBERS Future Income Annuity

Where it can work best: This annuity may be a good choice for you if you are:- Anticipating a long life span

- Need retirement income in the distant future

- Are seeking a source of guaranteed lifetime income down the road

- Have a shorter life expectancy

- Need to keep your money liquid for potential emergencies

- Do not plan to use the lifetime income feature

In Summary

Because deferred income annuities (DIAs) will oftentimes provide a higher amount of income (as versus an immediate annuity), these financial vehicles can be attractive to many who are retired or who are approaching that time in their lives. But, just as you would likely do before making any other high ticket purchase, you must understand whether or not the product is appropriate for you, as annuities are not a one-size-fits-all vehicle. And, if you find out after you’ve committed that it really is not right for you, it could be quite an expensive mistake. If you are still leaning towards purchasing the CUNA Mutual MEMBERS Future Income Annuity, you can be assured that you’ll have a guaranteed income stream in the future – and if you choose the lifetime income option, you will have income for as long as you may need it. However, even with all of these nice financial guarantees, this particular annuity could quite possibly still fall somewhat short – and there very well could be a better alternative out there for you. In reality, the only way to truly know if this annuity may perform the way you want it to is to have it tested. We can do that for you by running the numbers through our annuity calculator, and we can then provide you with a spreadsheet showing the results. In order to receive this information, just simply contact us via our secure online contact form here.Do You Still Have Additional Questions About the CUNA Mutual MEMBERS Future Income Annuity?

We know that this annuity review has run a bit on the lengthy side. Yet, we feel that it is always much better to provide a bit “too much” information that not to provide you with enough. With that in mind, if you found this review to be beneficial, please feel free to forward it on and share it with anybody whom you think might also benefit from it. On the other hand, if this review has caused some confusion about this annuity – or even about the way that DIAs work in general – please let us know that, too. In addition, if there are any other annuities that you do not see in our annuity database that you would like to see reviewed, please contact us via our secure contact form and provide us with the name (or names, if there is more than one) of the annuity you are interested in knowing about. Best, The Annuity Gator P.S If you would like to read more of our CUNA Mutual annuity reviews here are some links to check out:- Independent Review of the CUNA Mutual MEMBERS Single Premium Immediate Annuity

- Independent Review of the CUNA Mutual MEMBERS Index Annuity