What’s Covered In This Review

In this review, we’ll be going over the information on the Fidelity Investment Life Insurance Company’s Personal Retirement Variable Annuity, such as:

- Product Type

- Fees

- Current Rates

- Realistic Long-Term Expectations

- How the Annuity Is Best Used

- How the Annuity is Most Poorly Used

Annuities can be complex. That’s where having an Annuity Investigator who loves math comes in.

We make the complex, simple.

What you will likely notice, is that like just about any other annuity, the Personal Retirement Variable Annuity from Fidelity Investment Life Insurance Company can perform very well in certain areas. But, there can be some other areas where it may not do all that well for you, depending on your specific financial goals, time horizon, and risk tolerance.

If this is the first time you have visited our website and you aren’t familiar with us, we are fee only financial planners – so we do not get paid to sell our clients annuities, nor do we sell these products.

However, unlike other fee-only financial planners, we do feel that these products can provide some investors with a key piece of their overall financial planning strategy – as long as they are used in the proper manner. Because our pay is not tied to the sale of annuities, we have no real incentive for or against them. Therefore, our views are completely impartial and unbiased.

If you have recently attended an annuity seminar or workshop, you may have – in return for a complimentary lunch or dinner – already head some of the details about this, or another, annuity. Attending that even may even be what has brought you here to our site in search of additional details.

In your quest for annuity information, you may also have run across some of the other websites out there on the Internet that tout the benefits of their products. In fact, some of these sites make some pretty bold claims, such as:

- Highest annuity rates

- Lowest fees

- Top rated annuity companies

- Get your quote now!

Look familiar?

While these sites may be able to provide you with some of the information that you need, we dare say that the website that you are on right now will provide you with much more of the in-depth information that is required for making a good, solid purchase decision. This can be helpful, as many of the other “copycat” annuity sites will often times only give you the good, but not the bad or the downright ugly.

We will, though, primarily because we feel that you have to have the entire picture in order to truly make a decision that is right for you – and, because you can get “locked in” to an annuity, if you buy one of these products and then decide that you want to get out, it can cost you a great deal in surrender fees.

So if you’re ready to begin the review, let’s get started!

Fidelity Investment Life Insurance Company’s Personal Retirement Variable Annuity at a Glance

| Product Name | Personal Retirement Variable Annuity |

|---|---|

| Issuer | Fidelity Investment Life Insurance Company |

| Type of Product | Variable Annuity |

| Standard & Poor's Rating | |

| Phone Number | (800) 343-3548 |

| Website | https://www.fidelity.com/annuities/overview |

Opening Thoughts on the Structured Capital Strategies Annuity

In general, a variable annuity is designed for accomplishing two key goals. One is to grow principal, and the other is produce retirement income in the future. However, in reality, these types of annuities really are not all that great at producing income, because of the risk that they present to the investor, as well as to the insurance company that offers them.

In fact, due to the fact that a variable annuity’s value can fluctuate so much, the insurance company that offers it can only actually guarantee less income than the more safe alternatives like fixed annuities can offer. Therefore, for each dollar that is invested into a variable annuity, it is going to provide you with less income than a fixed annuity would for the exact same money. Given that, if your main goal in purchasing an annuity is to ultimately use it for producing retirement income, then a variable annuity is not likely going to be the best option.

When it comes to the investment aspect of variable annuities, these vehicles can provide investors the opportunity of unlimited growth. However, along with that can also come downside risk – and in some cases, a substantial amount of downside risk.

Variable annuities are also known for having a significant amount of charges and fees – not just up front, but also throughout the time that an investor owns the product. One reason for this is the fees that are charged by the variable annuity itself. But, because variable annuities are also invested in mutual funds, you will typically also have to pay the fees that each of the funds charges, too.

Throughout the years, investors who have had funds invested in the market have been worried about not meeting their retirement goals. This has been due in large part to the great amount of volatility of the market – which in turn, gives way to the potential loss of investors’ principal.

The Personal Retirement Variable Annuity from Fidelity has the ability to help with building long-term wealth with a tax-deferred growth strategy. As with most other annuities, this vehicle is designed to help investors with managing a portion of their portfolio’s tax exposure by allowing tax-deferred growth.

There are also more than 55 managed funds to choose from – both from Fidelity and from other non-Fidelity alternatives – many of which are rated as 4- and 5-star by Morningstar.

Investors are also allowed to rebalance funds within the annuity with no tax consequences. And, unlike investing in a traditional IRA, there are mandatory required minimum withdrawal stipulations with this product.

Before we get into the gritty details, here is some necessary legal information that we need to disclose…

This is an independent annuity product review and it does not constitute any type of recommendation to purchase or sell an annuity. Fidelity has not endorsed this review in any way, and I do not receive any compensation for providing this review. This information is meant to be an independent opinion so that readers may see my personal perspective when determining the potential advantages and/or drawbacks of this particular financial vehicle, and how it may or may not fit into their specific financial portfolio. Prior to purchasing any type of investment or investment product, it is important to pursue your own due diligence and to consult with a competent and properly licensed financial professional before moving forward. This way, you can more precisely ensure that the product and/or service fits in with your individual circumstances. All names, trademarks, and materials that were used in this annuity review are the property of their respective owners.

How Fidelity Describes the Personal Retirement Variable Annuity

The Fidelity Personal Retirement Variable Annuity was designed as a tax-advantaged savings vehicle.

With this annuity, there are no additional riders or other insurance options that are typically found in other annuity options. This can help to reduce or eliminate at least some of the annuity’s fees.

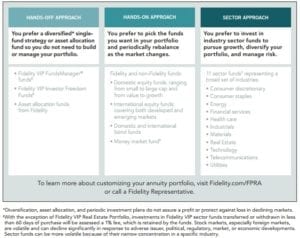

Investors can still “customize” this annuity to some degree – but for those who do not want to choose their own funds, there are options for that, as well. For example, there is a “hands on” approach option, where the investor is able to pick the funds that he or she would like to have in the portfolio. The investor can also periodically rebalance as the market changes and/or as their needs change over time.

With the hands off option, investors can choose from several different alternatives to investing in, such as the Fidelity VIP FundsManager funds, the Fidelity VIP Investor Freedom Funds, or the Asset allocation funds from Fidelity.

Alternatively, there is also a “hands off” approach. Here, the investor gets a diversified single fund strategy or asset allocation funds so that they do not need to worry about building their own portfolio.

With this option, there are both domestic and international equity and bond funds, both Fidelity and non-Fidelity. There is also a money market alternative if an investor wishes for additional safety.

A third option with the Personal Retirement Variable Annuity from Fidelity Investment Life Insurance Company is the “sector approach.” With this option, if an investor prefers to invest in industry sector funds in order to pursue growth, diversify their portfolio, and/or manage risk, they can do so with this option.

With the sector approach, there are eleven different sector funds, which represent a wide range of industries, such as energy, health care, real estate, technology, utilities, and financial services.

How an Advisor Might Pitch this Annuity

How an Advisor Might Pitch this Annuity

If you’ve been offered the Fidelity Investment Life Insurance Company’s Personal Retirement Variable annuity by a commissioned insurance or investment advisor, then it is likely that they will be focusing on the positives of this annuity, while possibly not highlighting the aspects of this annuity that could be considered drawbacks. One such drawback is the risk that the investor takes when purchasing a variable annuity.

Today, variable annuities are not nearly as popular as they were several years ago. Rather, index annuities – which offer the opportunity for index-linked return, along with the safety of principal – have become much more sought after. One reason for this is because they can guarantee safety, yet provide a higher return than a regular fixed annuity.

With that in mind, it is probable that a financial professional will key in on the ability of a variable annuity to possibly provide a higher return, as well as diversity in investment options. Also, because people are living so much longer today, one primary fear that many retirees have is that of running out of money. The guaranteed lifetime income from an annuity can help to rid that fear.

This annuity also comes from an extremely financially stable and strong company. Fidelity has roughly 25 million customers worldwide, and the company is estimated to have more than $2.1 trillion in assets under management.

However, if one of your key reasons for purchasing an annuity is for the income benefit, it is highly recommended that you first take into consideration the projected income from this annuity, as there may be other products out there that can offer a higher level of guaranteed income – along with more protection from a downward moving market.

Because there is no “perfect” product or investment, it is important to know clearly what your priorities are right from the beginning. This is especially the case before you move forward with signing an annuity contract because once you are in, it can be difficult – and costly – to get out.

It can be difficult to know which annuity will be the best one for you and your specific circumstances. But it can be helpful to know some key tips when shopping for this type of product. in order to obtain our free annuity shopper’s guide so that you can feel more confident in your decision going forward.

What About the Fees?

Overall, variable annuities tend to be some of the more costly investment vehicles that are available in the market today. And, while the Personal Retirement Variable Annuity from Fidelity has made some provisions to keep fees lower than similar annuities, it is still important to know what and how much you can be charged.

For example, in this case, according to the prospectus, the Personal Retirement Variable Annuity has a 0.25% annual annuity charge. There is also an administrative charge. This is assessed against each contract’s assets at an effective annual rate of 0.10%.

While the annuity doesn’t have a surrender charge per se for early withdrawals of more than 10% of the contract’s value, it does incur what it refers to as a short-term redemption fee. There are several of the annuity’s investment options that invest in funds which impose a short-term redemption fee. These too can differ, depending on the fund or funds.

In addition to the charges from the annuity itself, there are also expenses and charges that can be incurred by the mutual funds that are invested in the annuity. These can differ by company and fund type.

The Annuity Gator’s End Take on the Fidelity Personal Retirement Variable Annuity

Where it works best:

There is no one-size-fits-all investment that is right for everyone. But, if you are leaning towards the Fidelity Investment Life Insurance Company Personal Retirement Variable Annuity, then it could be a viable option for you if you are seeking the ability to earn a higher rate of return than a fixed annuity, while also taking guaranteed lifetime income in the future.

Where it works worst:

Certainly with most variable annuities, because of their added risk that investors may incur, these are not good options for those who are looking to keep their principal safe, and/or who do not have a high tolerance for risk.

Also, the Fidelity Personal Retirement Variable Annuity does not offer a myriad of bells and whistles (i.e., riders), so if you are seeking more options than that of tax-deferred growth and lifetime income, then this annuity isn’t like the one for you. Likewise, if you don’t plan to use the lifetime income feature on this annuity, then there could also be a better alternative out there.

In Summary

When considering any type of financial investment, it is essential that you determine first what your overall goals are. That way, you will be much better able to go through the process of eliminating the options that won’t fit in with your plan.

In the case of the Fidelity Investment Life Insurance Company Personal Retirement Variable Annuity, there can definitely be some attractive features, such as the many different equity investment options, and the ability to diversify your holdings within the annuity.

Likewise, you can also obtain tax-deferred growth of your money – which in turn, can allow your funds to grow and compound exponentially over time. Plus, you can count on at least some amount of guaranteed income down the road.

But, in order to really know if this particular annuity will be a good fit for you is to have it tested. We can do this for you. The calculator and resulting spreadsheet are free. So, if you are interested, please let us know and we will be happy to run the figures for you.

Have Any Additional Questions on the Fidelity Investment Life Insurance Company Personal Retirement Variable Annuity? Did You Notice Any Mistakes?

Admittedly, this annuity review ran a tad bit long – so we truly appreciate you sticking with us here. Our thought is that we would much rather provide you with “too much” information than not enough.

If you did feel that this annuity review was helpful, then, by all means, please feel free to forward it on to anyone else that you think might also benefit from it. Alternatively, if this review brought forth, even more, questions, then please also let us know.

Also, as many humans do, we can at times make mistakes. So, if you happened to notice any mistakes in this review, please send us a message here via our secure online contact form so that we can make the corrections as soon as possible.

Any other annuities that you’d like to see reviewed?

If there are any other annuities that you would like to see reviewed, please let us know that, too, and we will get our team of qualified annuity “geeks” on the case and have more reviews available on our website soon.

Best,

The Annuity Gator

2 Comments

You always do a great job of explaining things.

I can definitely see where you’re coming from and I appreciate the insight.

I shared this on Facebook and my friends seemed to enjoy it too.

Keep it up!

Hi – Thank you for your message, and for sharing! If we can help further, please feel free to reach out to us directly at (888) 440-2468, or through our secure online contact form at https://www.annuitygator.com/contact/. Best! The Annuity Gator