What will we cover in this review?

In this annuity review, we’ll be covering the following information on the Pacific Life Insurance Company’s Pacific Index Foundation Fixed Indexed Annuity:- Product type

Fees

Fees- Current rates

- Realistic long-term return expectations

- How this annuity is best used

- How it is most poorly used

Annuities can be complex. That’s where having an Annuity Investigator who loves math comes in. We make the complex, simple.

If you’ve been considering the idea of purchasing an annuity so that you can grow your money in a tax-advantaged manner, but without the concern of losing money in a stock market downturn, then a fixed indexed annuity like the Pacific Life Pacific Indexed Foundation fixed indexed annuity (FIA) could be a good option for you. However, prior to going out and making a long term commitment to this – or to any other – financial product, it is important to be sure that you have a good understanding of how it works, and how it may, or may not, work for you and your specific financial goals. Throughout the past decade or so, annuities have become much more popular with those who are saving for retirement, as well as those who are entering into this stage in their lives. One of the key reasons for this is because annuities can provide a stream of guaranteed income, regardless of how long you may need it. Also, because the stock market has been particularly volatile since the 2008 recession, a fixed indexed annuity, in particular, can help with growing your nest egg, while at the same time keeping it safe. Due in large part to this growth in annuities’ popularity, there are many more insurance and financial advisors who are offering these products. This, however, is not necessarily such a good thing, because even though most financial professionals will work to do what’s right for their clients, not everyone understands the intricacies of annuities – and because of that, investors don’t always end up getting what they thought they had purchased. As a result, it is essential that you know exactly what it is that you’re getting into with your retirement money, as locking yourself into the wrong annuity could end up being a time-consuming and costly endeavor if you decide you want out.

Annuity and Retirement Income Planning Information that Can Be Trusted

If this is the very first time that you’ve visited our website, we’d personally like to welcome you to AnnuityGator.com. We make up a team of experienced financial pros who are dedicated to providing both comprehensive and non-biased annuity reviews. We’ve been offering these in-depth reviews for quite a few years now – much longer than our competitors have been – and because of this, we have come to be known as a highly trusted source of annuity information. If your search for annuities has been conducted primarily via the Internet, then it is likely that you have come across many conflicting details about these financial products. This isn’t really all that surprising, though, because there is a multitude of different annuities in the market today, and there are numerous opinions about them. Although there are a number of very good websites out there that are focused on marketing their annuities online, the reality is that some of these websites will work hard at luring you in by touting some pretty impressive claims, such as:- Highest guaranteed income payouts

- Top rated annuity carriers

- Guaranteed income for life – no matter how long you need it

- Lowest annuity fees

The Pacific Life Insurance Company Pacific Index Foundation Annuity at a Glance

| Product Name | Pacific Index Foundation |

|---|---|

| Issuer | Pacific Life |

| Type of Product | Fixed Indexed Annuity |

| S&P Rating | AA- |

| Phone Number | (800) 772-4448 |

| Website | www.pacificlife.com |

Opening Thoughts on the Pacific Life Index Foundation Fixed Indexed Annuity

Pacific Life has been helping clients to grow and protect wealth for roughly 150 years. Throughout this time, the company has grown – both in terms of client base as well as via its assets under management. The company held approximately $158 billion in total assets as of year-end 2017, as well as more than $11.2 billion in equity. With more than $9.4 billion in operating revenues and operating income in excess of $774 million, Pacific Life is more than able to uphold its promises to policyholders. Because of its strong financial footing, as well as its timely payout of policyholder claims, Pacific Life has earned high ratings from the insurer rating agencies, including the following (as of 2018):- A+ (Superior) from A.M. Best Company

- A+ (Strong) from Fitch Ratings

- A1 (Good) from Moody’s Investor Service

- AA- (Very Strong) from Standard & Poor’s

Before we get into the gritty details, here are some legal disclosures…

This is an independent product review, not a recommendation to buy or sell an annuity. Pacific Life Insurance Company has not endorsed this review in any way, nor do we receive any type of compensation for providing this review. This review is meant to be an independent review at the request of readers so that they may see our perspective when breaking down the positives and negatives of this particular annuity. Prior to purchasing any type of investment or insurance product, it is important that you do your own due diligence and that you consult a properly licensed professional if you should have any specific questions that relate to your individual circumstances. All names, marks, and materials that were used for this review are the property of their respective owners. For more information on how to compare annuities in order to determine which one may be right for you, click here to obtain our free annuity report.How Pacific Life Insurance Company Describes the Pacific Index Foundation Annuity

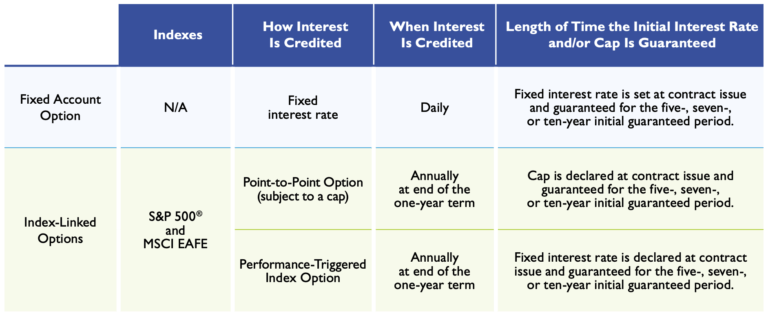

Based on its product literature Pacific Life Insurance Company describes the Index Foundation as a deferred, fixed indexed annuity. With this FIA (fixed index annuity), you can protect the principal inside of the contract, while at the same time having the opportunity to attain a nice return that is based on the performance of the underlying market index(es). Then, when you are ready to start drawing income from the annuity, you can rely on a lifetime stream of incoming cash flow for the remainder of your life – regardless of how long that may be. This, in turn, can definitely help to alleviate the concern about running out of income before “running out of time”. As the owner of a Pacific Life Pacific Index Foundation annuity, you won’t lose principal when the underlying index performs poorly in a given time period. Rather, during these times, your account will just simply be credited with 0%. (So, while there is no gain at that time, there is also no loss…which is something that many investors would love to have had during the recession of 2008!) Also, during your accumulation period, you can lock in a guaranteed rate of return for a set period of time in the fixed account – which in this case can be for five, seven, or even for a full ten years. Also, your gains will be locked in, never to be lost due to future market volatility. The index options that are tracked with the Pacific Life Insurance Company’s Pacific Index Foundation annuity include the S&P 500 and the MSCI EAFE Index (Europe, Australia, and the Far East). Likewise, if you opt to make an allocation to an index-linked option within the Pacific Index Foundation annuity, there are actually two different methods that you may choose from for the interest to be added to your account. These include the:- Point-to-Point Option: With the point-to-point option, interest is credited annually, based on the return of the underlying index over one contract year, up to a maximum (that is referred to as a “cap”). If the index return ends up to be negative during a given period, there will be no interest credited.

- Performance-Triggered Index Option: Here, a declared, fixed interest rate is credited when triggered by a flat or positive index return over one contract year. In this case, too, if the index return comes out to be negative, no interest will be credited.

For a full rundown of all the fine print associated with the Pacific Life Insurance Company’s Pacific Index Foundation annuity, you can check out the updated product literature HERE.

For a full rundown of all the fine print associated with the Pacific Life Insurance Company’s Pacific Index Foundation annuity, you can check out the updated product literature HERE.

How Insurance or Financial Advisors Might “Pitch” This Annuity

The continued volatility of the stock market has led many to consider placing retirement savings into a fixed indexed annuity. Because fixed indexed annuities can offer the opportunity for a higher return than a regular fixed annuity – while also offering safety of principal – many insurance and financial advisors will pitch these products as offering the best of both worlds. The ability to receive an ongoing income stream in retirement can essentially make these types of annuities the “triple crown.” Yet, if you are being offered the Pacific Life Pacific Index Foundation fixed index annuity by an insurance or financial advisor who gets paid only when he or she actually sells something, then you may want to know whether or not this is the best product for you – or for them! You also need to be careful when investing in any indexed annuity product, as in many cases, the index’s return will not include the payment or the reinvestment of dividends in the calculation of its performance. With that in mind, even though some indexed annuities in some cases may be able to provide a higher return than other “safe” alternatives like CDs or money market accounts, it is more likely – especially in our current low interest rate environment today – that even the money that is in an indexed annuity will provide a return that’s closer to 2 or 3%.What About Any Fees on the Pacific Life Pacific Index Foundation Annuity?

It can be quite a feat today to find any insurance or financial product that won’t charge at least some amount of fee in order to put your money to work. The Pacific Index Foundation annuity is no different. Here, for instance, if you need access to more than 10% of your contract’s value while the annuity is still within its “surrender charge period,” you will be hit with a fee on any money withdrawn that is over and above that amount. In the case of this annuity, the length of the surrender charge period corresponds with the length of the rate guarantee period – so, the longer your guarantee, the longer you’ll have to wait to withdraw more than 10% of your account value without a penalty.The Pacific Life Pacific Index Foundation Annuity Surrender Charge Schedule

| Year: | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11+ |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 5-yr rate guarantee | 9% | 8% | 8% | 7% | 6% | 0% | |||||

| 7-yr rate guarantee | 9% | 8% | 8% | 7% | 6% | 4% | 4% | 0% | |||

| 10-yr rate guarantee | 9% | 8% | 8% | 7% | 6% | 4% | 4% | 3% | 2% | 1% | 0% |

The Annuity Gator’s End Take on the Pacific Life Pacific Index Foundation Fixed Index Annuity

Where it works best: The Pacific Index Foundation fixed indexed annuity could be a viable choice for you if you are seeking the following:- Protection of your principal

- The potential for higher growth than with a regular fixed annuity or CD

- A lifetime stream of guaranteed income

- Want access to more than 10% of your contract value within the first several years (depending on the length of the surrender charge)

- Do not plan to use the guaranteed lifetime income feature

In Summary

There can really be a long list of factors to consider if you are considering the purchase of an annuity. In any event, however, an annuity should always be considered as a long term financial commitment. With a fixed indexed annuity such as the Pacific Life Insurance Company’s Pacific Index Foundation annuity, you can definitely rely on your principal being safe from the constant ups and downs of the stock market. You can also be sure that you can receive an ongoing income in the future, regardless of how long you may need it (provided that you choose the lifetime income option). Given that, the Pacific Index Foundation annuity can, in fact, offer some very nice benefits. However, on the other side of the coin, this annuity can also fall somewhat short – and there may be a better alternative out there for you. If, after you read through this annuity review, you still have some questions and/or concerns regarding the Pacific Index Foundations fixed indexed annuity – or for that matter, any annuity – please feel free to reach out to us directly via our secure online contact form here.Do You Have Any Additional Questions? Did You Notice Any Mistakes in this Annuity Review?

We know that this review was a bit on the long side. And for that, we truly appreciate you sticking with us through it all. But our feeling is that we would much rather “err” on the side of being too long than on not providing enough of the details. If you do still have any questions or concerns and you would like to discuss them with an annuity expert, then please contact us through our online form. Also, if there are any other annuities that you would like to see reviewed here on our website, then just simply let us know the name (or names) of those products, and our team of annuity “geeks” will get on it. Best, The Annuity Gator P.S If you would like to read more of our Pacific Life annuity reviews here are some links to check out:- Independent Review of the Pacific Life Frontiers ll Fixed Deferred Annuity

- Independent Review of the Pacific Life Expedition Fixed Deferred Annuity

- Independent Review of the Pacific Life Secure Income Deferred Income Annuity as a QLAC

- Independent Review of the Pacific Life Core Protect Advantage Variable Annuity

- Independent Review of the Pacific Life Pac Mariner 7 Year Guaranteed Rate (MYGA) Annuity

- Independent Review of the Pacific Life Pacific Index Choice 6 Fixed Indexed Annuity

- Independent Review of the Pacific Life Pacific Frontiers II, 1 Year Guarantee Fixed Annuity

- Independent Review of the Pacific Life Pacific Odyssey Variable Annuity