What Will We Cover in this Annuity Review?

In this annuity review, we will be covering the following details regarding the Security Benefit Rate Track 7-Year MYGA Fixed Annuity:

- Product type

- Fees

- Current rates

- Realistic long term return expectations

- How this annuity is best used

- How it is most poorly used

Annuities can be complex. That’s where having an Annuity Investigator who loves math comes in.

We make the complex, simple.

If you have been seriously thinking about purchasing a fixed annuity because you want to know that your principal will be safe and that you will also obtain a guaranteed lifetime income in retirement, then the Security Benefit Rate Track 7-Year MYGA fixed annuity may be a viable option for you.

One reason for this is because this annuity can provide you with a rate guarantee for seven years – and, if interest rates rise during that time, you may even get a higher return on your money. It can also provide you with a lifetime income stream in the future, so you can alleviate the worry about running out of income before “running out of time.”

However, even as enticing as these benefits might sound, you really shouldn’t go out and purchase this – or any – annuity unless or until you have an in-depth understanding of just exactly how the product works, and how it may or may not work for you.

Throughout the past decade or so, due in large part to the constant ups and downs of the stock market, fixed annuities have become quite popular. This is especially the case for those who are retired, or who are in the process of preparing for that time in their lives. With their income guarantees, as well as the fact that your principal is kept safe, fixed annuities may seem to be the best of all worlds for investors.

But, just like with any other type of annuity, you need to proceed with caution. For example, the Security Benefit Rate Track 7-Year MYGA (multi-year guarantee), is an annuity that has a few “moving parts” – and along with these can come a plethora of small print that you really need to know about before committing a large chunk of money to this product.

Annuity and Retirement Income Planning Information You Can Trust

If this is your first visit to our website, we would like to officially welcome you to AnnuityGator.com. We are a team of experienced annuity professionals who focus on offering comprehensive – and unbiased – annuity reviews.

We’ve been at this for quite some time now – and much longer than our competitors. Because of this, we have come to be known as a very trusted source of annuity information online. However, over the past several years, a number of other “copycat” sites have also started springing up all over the Internet.

If you’ve spent any amount of time searching for information about annuities online, it is likely that you have also run across some highly conflicting details about these products. This, however, is not all that surprising, as there are many, many annuities out there in the market, and everyone seems to have differing opinions about them.

It is also likely that you have attended an annuity seminar in the recent past where the presenter offered you in-depth information about the Security Benefit Rate Track 7 or some other, similar annuity. If you wanted to know more, this seminar may even have been the reason that you have ultimately ended up on our website today.

In your search for annuity information online, you may also have come across some of the other sites that discuss annuities online. While these may initially seem informative, many of these websites are actually just trying to lure people in – in order to collect your contact information – by making some pretty bold claims, such as:

- High Annuity Income Payouts

- Guaranteed Income for Life

- Top-Rated Annuity Carriers

- Low Fees

Sound familiar?

As nice as these claims may be, though, it is all the more important for you to verify whether or not they are actually valid before moving forward with the purchase of an annuity – just as you would likely do prior to buying any other type of high-dollar product or service.

If you are in fact seeking additional details regarding the Security Benefit Rate Track 7-Year MYGA fixed annuity, you are definitely in the right place. In fact, we dare say that our website is the only place online where you can truly be able to obtain all of the in-depth information that you’ll need for making a well-informed buying decision (or alternatively, making the decision to forgo this particular annuity and move on to something else).

As you read through this annuity review, you will find that we don’t just lay out the nice, rosy advantages of the product, but we also give you details about what could be considered some serious drawbacks, too. We don’t do this to scare you, but rather to give you the whole picture, as we firmly believe that knowing everything is the only way to make a truly informed financial related decision.

With that in mind, we also want to be clear in that we fully believe that an annuity can be a great financial vehicle for some people – provided that it fits in well with your short- and long-term financial goals.

So, with that being said, if you’re ready to proceed, then let’s go ahead and get started!

Security Benefit Rate Track 7-Year MYGA Fixed Annuity at a Glance

| Contract Year | 1 | 2 | 3 | 4 | 5 | 6+ |

|---|---|---|---|---|---|---|

| Charge % | 9 | 8 | 7 | 6 | 5 | 0 |

Opening Thoughts on the Security Benefit Rate Track 7-Year MYGA Fixed Annuity

Security Benefit is a leader in the United States retirement market. As of March 2017, the company had more than $35 billion in assets under management – which equated to a 14% increase in asset growth over 2015.

This company’s key strength lies in specialty markets – particularly overall fixed annuity sales. Security Benefit has applied its core capabilities and investment expertise to cultivate a full range of innovative products in order to help nearly 1/2 million clients retire comfortably – regardless of where they are on their retirement path.

Throughout the past several years, fixed annuities have grown in popularity, especially for those who have a goal of keeping their principal safe from market fluctuations, as well as those who want to know that they can count on an income for the remainder of their lives.

But, even though these features and guarantees might initially sound ideal, the truth is that if something sounds too good to be true, it just might be. So, given that, it is important that you gather as many of the details as you possibly can before you move forward with purchasing this, or any other, fixed annuity.

Before we get into the gritty details, here are some necessary legal disclosures…

This is an independent annuity product review. It is not a recommendation to purchase or to sell an annuity. Security Benefit has not endorsed this review in any way, nor do we receive any type of compensation for providing this review. This annuity review is meant solely to be an independent review at the request of our readers so that they may see out perspective when breaking down the positives and the negatives of this particular annuity. Before purchasing any type of insurance and/or investment product, it is important that you do your own due diligence, and that you consult a properly licensed professional if you should have any specific questions that relate to your individual situation. All of the names, marks, and materials that were used for this annuity review are the property of their respective owners.

For more information on how to compare annuities in order to determine which one may be the best for you and your financial circumstances, to obtain our free annuity report.

How Security Benefit Describes the Rate Track 7-Year MYGA Fixed Annuity

The Rate Track 7-Year MYGA fixed annuity from Security Benefit Life is described as “a new concept in fixed annuities,” that offers a floating rate of interest where you can benefit if interest rates rise during the guarantee period of the contract.

Basically, with a rate track annuity, your principal is safe, and your money – while guaranteed a set rate for seven years – can also attain a better return if interest rates are to rise during that time.

This differs from other types of annuities, such as MYGA / multi-year guaranteed annuities, and even regular fixed annuities, that lock in a rate for a certain number of years, even if interest rates rise during that time period.

In other words, if you placed money in a regular fixed annuity or similar fixed savings instrument over the past few years, you may have had a nice safe rate, but you weren’t likely able to increase your return over time. So, while you were protected from any loss if rates went down, you also did not have the opportunity to receive any increase in return if interest rates went up.

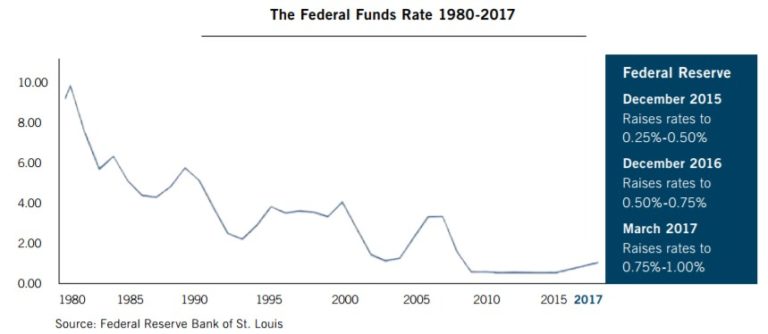

So, if you own this annuity, during the guarantee period of seven years, the interest will be calculated and credited on the combination of a fixed interest rate – the Guarantee Period Base Rate – and a floating rate, based on the 3-month ICE Libor USD rate (LIBOR), which has historically tracked the federal funds rate. The floating rate resets annually on the contract anniversary date as the LIBOR rate changes.

At the end of the seven year guarantee period of your contract, you can do either of the following:

- Take no action – and your money will automatically be allocated to a one-year term at a rate of interest that is set by Security Benefit at that time, or

- Withdraw all or a portion of your money from the contract.

The annuity also has a couple of other features on it, such as a nursing home waiver, and a terminal illness waiver. To check out the full product brochure for more details, go here.

How an Advisor Might “Pitch” This Annuity

Today, because the market downturn of 2008 is still somewhat fresh in peoples’ minds, keeping principal safe is a big concern. When it comes to fixed annuities, then, an insurance or financial advisor is likely to key in on the safety that you can get – and with this annuity, in particular, the proverbial icing on the cake is the fact that not only can you lock in a certain guaranteed rate, but your rate can increase if interest rates rise during that time period.

When you’re talking about lots of guarantees, though, it is important to keep in mind that somewhere along the line, there will be some tradeoffs to make. And when focusing on the Security Benefit Rate Track 7-Year MYGA annuity in particular – even though you could earn more than the guaranteed rate, the reality is that you still may not be able to beat, or even meet, the rate of inflation. Because of this, you would still need other options for increasing your savings and/or your future income if you want to keep your retirement income rising enough to meet future living expenses.

Also, you may also have the opportunity to access your money free of surrender charges if you are diagnosed with a qualifying terminal illness, or if you become confined to a nursing home. Here, too, you need to know just exactly what the fine print says. That is because in this case, the surrender charges are only waived if you request a withdrawal after the third contract anniversary of owning the annuity. Plus, depending on your state of residence, these benefits may not even be available to you at all.

What are the Fees Associated with the Security Benefit Rate Track 7-Year MYGA Fixed Annuity?

Just as is the case with most other insurance and financial products, there will be some charges and fees that are associated with the Rate Track 7-Year MYGA fixed annuity from Security Benefit.

Here, while there is no up-front sales commission, you may run into some pretty hefty surrender charges – particularly if you withdraw more than 10% of your annuity’s contract value during the first full seven years of owning the annuity.

Security Benefit Rate Track 7 MYGA Fixed Annuity Surrender Charge Schedule

| Product Name | Mariner 7 Year Guaranteed Rate MYGA |

|---|---|

| Issuer | Pacific Life |

| Type of Product | Multi-Year Guaranteed Annuity (MYGA) |

| S&P Rating | AA- |

| Phone Number | (800) 772-4448 |

| Website | www.pacificlife.com |

The Annuity Gator’s End Take on the Security Benefit Rate Track 7-Year MYGA Fixed Annuity

Where it works the best:

The Security Benefit Rate Track 7-Year MYGA Fixed Annuity may be right for you if:

- The interest rate for money you have in a bank savings or CD does not compare favorably to the interest rate potential that this annuity can offer

- You can put money into the annuity for a committed amount of time with the option to withdraw up to 10% per year free of surrender charge (if needed)

- You would like to accumulate more interest because you have a tax-deferred product rather than paying taxes on the interest in the same year in which it is credited

- You want the peace of mind in knowing that you can access your money free of surrender charges if you become terminally ill or confined to a nursing home facility.

Where it works the worst:

This particular annuity may not be right for you if:

- You want the opportunity to earn an even higher rate of return in order to keep better pace with future inflation

- You want to access more than just 10% of the contract’s value each year

- You do not plan to use the lifetime income feature

In Summary

There are a number of important concerns to keep in mind when you are saving for retirement. For instance, you want to be sure that your funds are earning a nice return, but that they are also safe from potential market downturns. It is also essential to know that you will have a reliable stream of income in retirement – regardless of how long you may need it.

If you are considering the purchase of the Security Benefit Rate Track 7-Year MYGA annuity, then you can be assured that your principal will be safe and that you will have an income stream in retirement that will continue for the remainder of your life.

However, even with these great attributes, the Rate Track 7-Year MYGA annuity from Security Benefit could still fall somewhat short – and quite frankly, there may just be a better alternative out there for you, especially if you are seeking the opportunity for an even better return.

In any case, the only want to truly know how this annuity may perform based on your specific situation is to have it tested. We can do this for you by running the numbers through our annuity calculator, and we can then provide you with a spreadsheet of the results. In order to receive this information, just simply contact us through our secure online form here and let us know.

Have Any Additional Questions? Notice Any Mistakes in this Review?

We realize that this annuity review was a tad bit longer. However, our feeling is that we would much rather “err” on the side of offering “too much” information than not enough. So, we do appreciate you sticking with us thus far.

If you found that this annuity review was helpful, then please feel free to forward it on to anyone else who you think might also benefit from it. Also, we realize that not everyone’s financial situation is the same. So, you may still have some questions about the Security Benefit Rate Track 7-Year MYGA fixed annuity – and if so, please reach out to us here and we will be happy to assist you further.

Are there any other annuities that you would like to have reviewed?

No problem! There are many annuities available in the market today. So, if you don’t see an annuity in our database that you would like to know more about, then just simply let us know the name of that annuity (or annuities, if there is more than one), and our team of annuity “geeks” will get to work on it!

Best,

The Annuity Gator