What will we be going over in this annuity review?

In this review of the Mass Mutual Stable Voyage 3 annuity, we will be covering the following topics:- Annuity type

- How the annuity works

- Advantages and potential drawbacks

- Fees

- Where the annuity may – and may not- be a very good fit

Annuities can be complex. That’s where having an Annuity Investigator who loves math comes in. We make the complex, simple.

If you are considering the purchase of an annuity because you want assurance that you’ll have a guaranteed stream of income in retirement, and that your money will be safe up until that time, then the MassMutual Stable Voyage 3 Fixed Deferred Annuity could be a viable option for you. This is because the Stable Voyage offers a fixed rate of return for a set period of time (in this case, three years) that you choose – and when the time comes to convert the annuity over into an income stream, you can also count on incoming cash flow for the remainder of your lifetime (regardless of how long that may be). However, before you run out and make a long-term financial commitment to purchasing this (or any other) annuity, it is essential that you first get a good idea of how it works, and how it may or may not work for you. Throughout the years, annuities have become more popular – especially with retirees and those who are approaching retirement. One reason for this is because they provide a guaranteed income stream, and they (deferred annuities) offer tax-deferred growth of your principal. With a fixed annuity, you also have the added bonus of assurance that your money will be safe – no matter what occurs in the stock market. This can help to alleviate the worry of a market correction impacting your future savings. Prior to signing on the dotted line, though, it’s a good idea to take a close look at an annuity’s fine print. That’s because these products can oftentimes have hidden charges and fees. And, while most insurance and financial companies do a great job of giving you all of the nice, rosy benefits that annuities offer, there can also be a few downfalls. With that in mind, it is much better to know these drawbacks now, as versus after you have already committed a large chunk of your savings to it. That’s where the Annuity Gator comes in.Annuity and Retirement Income Planning Advice You Can Trust

If you have never visited our website before, then please allow us to welcome you here to AnnuityGator.com. We are a team of annuity experts (“geeks”) who are focused on offering in-depth and unbiased annuity reviews. We’ve been at this for quite some time now – longer than our competitors – and because of that, we have come to be known as a trusted source of annuity information. But, just like anything that works well, there have also been a number of “copycat” websites that have popped up over the years. There are some websites out there that will make some pretty serious claims about the annuities they offer, with the primary intent of luring you in so that you part with your contact information. If you run across sites like this, be sure that what they are stating is actually true before you part with your hard-earned life savings. One big reason for this is because annuities can be difficult – and expensive – to get out of if you determine that the product you purchase isn’t really performing the way you expected it to. In order to be perfectly clear here, we want to say that we feel annuities can in fact be good products for some people – provided that they are in line with your overall financial goals and needs. That being said, let’s dive into this review!MassMutual Stable Voyage 3 MYGA Annuity at a Glance

| Product Name | Stable Voyage 3 |

|---|---|

| Issuer | MassMutual |

| Type of Product | MYGA (Multi-Year Guarantee Annuity) |

| A.M. Best Rating | A++ |

| Phone Number | https://justcall.io/calendar/ageup |

| Website | https://massmutual.com/ |

Opening Thoughts on the Stable Voyage 3 MYGA Annuity from MassMutual

MassMutual (Massachusetts Mutual Life Insurance Company) has nearly 170 years of experience under its belt in the wealth preservation and protection arena. As of year-end 2018, the company had roughly $255 billion in total assets. Headquartered in Springfield, Massachusetts, MassMutual is considered to be one of the leading mutual life insurance companies in the world. In early 2020, MassMutual approved a $1.7 billion estimated dividend payout for later in the year to be received by its eligible policyholders. While dividends are never guaranteed, MassMutual has regularly paid them out over the past century! Rated highly by all of the major insurer ratings agencies, MassMutual is considered to be strong and stable, and it has a good reputation for paying out claims to its policyholders. The company will likely continue to do so, particularly in the area of annuities, as these products have become much more popular over the past decade or so. Back in the early 1900s, average life expectancy was only in the neighborhood of 41 years old. Over the past 110 years, though, things have changed. In fact today, many people are living well into their 80s, 90s, and beyond. But, while this can allow you to spend more time enjoying your retirement years, it can be quite difficult to do without enough income. A fixed annuity can help you with this issue, because you can opt to receive income for the remainder of your life. And, a MYGA (Multi-Year Guarantee Annuity) can also provide you with some nice benefits during the “accumulation” period (i.e., before you convert the annuity to an income stream).Before we get into the in-depth details, we have some legal disclosures to present…

This is an independent annuity product review. It is not a recommendation to purchase or to sell an annuity. MassMutual has not endorsed this review in any way, nor do we receive any type of compensation for providing this review. This annuity review is meant solely to be an independent review at the request of our readers so that they may see our perspective when breaking down the positives and the negatives of this particular annuity. Prior to committing to the purchase of any type of insurance and/or investment vehicle, it is critical that you do your own due diligence, and that you also talk with a properly licensed professional if you have any questions that relate to your specific situation. All of the names, materials, and marks that have been used in compiling this annuity review are the property of their respective owners. For more details on how to compare fixed annuities so that you can decide which may be the best one for you, click here in order to obtain our free annuity report.How MassMutual Describes the Stable Voyage 3 Fixed Deferred Annuity

MassMutual describes its fixed annuities as financial vehicles that can provide you with predictability, liquidity, and even a death benefit. With an MYGA annuity like the Stable Voyage 3, the interest rate is locked in for three years. At the end of the initial three-year guarantee period, you may renew the contract again for either one, three, four, or five years. (If you do so, keep in mind that the surrender charge period will re-set. More on this further in the review). If you do not go with a new rate guarantee period, you have other options, which include either fully or partially annuitizing the contract (i.e., turning it into an income stream), or taking a full or a partial withdrawal from the annuity with no surrender charge penalty. As with other types of annuities, the growth that takes place in the account is tax-deferred, meaning that you won’t have to pay tax on the gains until the time of withdrawal. So, if you leave your money in the annuity for a while, you can generate growth in three ways – interest on the principal, interest on the interest, and interest on the money that would have otherwise been paid out in taxes. If the unexpected occurs and you pass away before you have converted the annuity over to an income stream, then your beneficiary will receive a death benefit. You may also withdraw up to 10% of the contract’s value each year without penalty – even during the surrender charge period. (We’ll get to that in a minute, too). A couple of additional features can be found on the Stable Voyage 3 annuity, including:- Nursing Home and Hospital Waiver – This feature allows you to withdraw some or all of the contract value without incurring a surrender penalty, provided that you are either confined to a licensed nursing home or that you are in an accredited hospital for at least 90 continuous days. (There may be other eligibility criteria, as well, depending on what state you reside in).

- Terminal Illness Waiver – With the terminal illness waiver, you may also withdraw some or all of the contract’s value if you become terminally ill during the accumulation phase of the annuity (i.e., before you convert the annuity to an income stream).

- Death Benefit – If you pass away during the annuity’s accumulation phase, the amount of the death benefit payment to your beneficiary will be equal to the contract’s value as of the date the insurance company receives proof of death and the beneficiary’s election of a payment method. (The beneficiary may opt to receive a lump-sum payment or installment payments over a set period of time). There may also be a death benefit paid out if you pass away during the annuity’s income payout period – depending on which annuity option you have chosen.

How an Insurance or Financial Advisor Might “Pitch” This Annuity

Given that life is filled with so many uncertainties, when you have the opportunity to receive a guarantee, it can be a nice benefit – particularly when they have to do with your financial options. With that in mind, when it comes to the MassMutual Stable Voyage 3 MYGA annuity, it is likely that an insurance or financial advisor would key in on the fact that you can obtain a guaranteed rate of interest for a set period of time, and that you can also count on a set amount of income from this annuity in retirement. However, whenever you have a guarantee presented to you, you could also find that there are certain “tradeoffs” that you need to accept in order to attain those benefits. This can be the case with the MassMutual Stable Voyage 3 Annuity. Here, for instance, initial 3-year rate guarantee period, matches up with the length of the surrender charge period. Plus, if you opt to lock in to another rate guarantee period after the initial three years have elapsed, the surrender charge period will also re-set. That can make it really difficult to get more than 10% of your money out for a long period of time. Also, when it comes to the nursing home and hospital waiver benefit(s), there are some guidelines that you must first meet in order to qualify for the surrender charge-free withdrawals. In this case, you would have to be in a licensed nursing home or accredited hospital for at least 90 days.What About Fees on the Stable Voyage 3 Annuity from MassMutual?

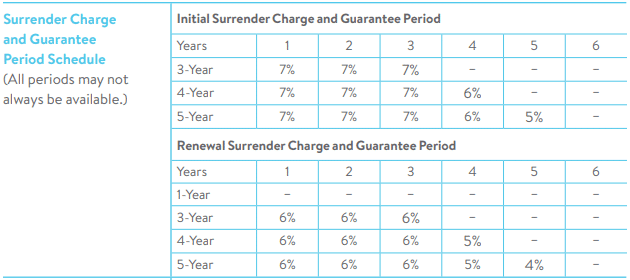

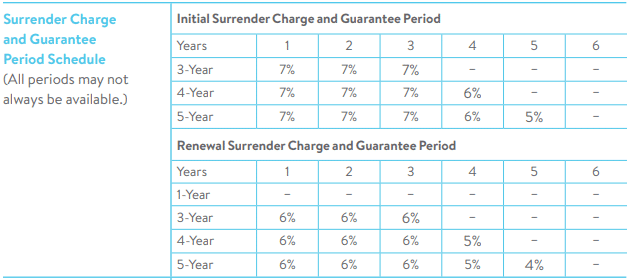

Annuities are known for charging fees – so you will find at least some on the Stable Voyage (although there are typically far more fees on variable annuities). In this case, there could be an annual administrative (or as MassMutual calls it, a Contract Maintenance) fee of $50 annually. (At this time, there is not – but MassMutual leaves the door open for that to change at any time). There is also the surrender charge to contend with. In this case, the Stable Voyage 3 annuity guarantees your interest rate for three full years, and the initial surrender charge corresponds to the 3-year period as well. If, however, you decide to renew the annuity down the road and lock in to another rate guarantee, the surrender charges will start all over again. Ouch!MassMutual Stable Voyage Annuity Surrender Charge Schedule

On top of that, you may also have to pay tax on any of the gain that is withdrawn – AND possibly also face an additional 10% early withdrawal penalty from the IRS.

The Annuity Gator’s End Take on the MassMutual Stable Voyage 3 Annuity

Where it works the best: The MassMutual Stable Voyage 3 MYGA Annuity may not be right for everyone, but it could be a good option if you are seeking:- A guaranteed rate of interest for a set period of time

- Safety of principal, regardless of what happens in the market

- A lifetime income that you can count on

- Want the potential for higher growth

- Need to access your money during the annuity’s surrender period (as well as the new surrender period if you opt to lock in your rate again after the initial rate period)

- Do not plan to use the lifetime income feature

In Summary

There is a long list of criteria that should be considered when you are thinking about the purchase of an annuity. These should include, but are certainly not limited to, how the annuity produces its return, how safe your money will be while inside of the contract, how the income will pay out, and whether or not there are any other features that will be beneficial to you now and/or in the future. If you’ve been considering the purchase of a deferred fixed annuity such as the MassMutual Stable Voyage 3, then you can certainly be assured that your money will be safe and that you will also be able to count on a steady stream of income for the rest of your life – regardless of how long that may be. However, there may also be some additional items that you have not considered – and the only way to really know if a particular annuity is going to be right for you is to have it tested. We can provide this testing for you, and can offer you a free, no-obligation, spreadsheet with the results. So, if this is something that is of interest to you, then all you need to do is simply reach out to us here via our secure online contact form.Still Have Questions? Notice Any Mistakes in this Annuity Review?

We know that this annuity review went a bit on the lengthy side, and for that, we do appreciate you sticking with us through it thus far. That being said, though, we feel like it is much more beneficial to provide readers with “too much” information than with not enough. So, if you found that this annuity review was beneficial to you, then please do feel free to forward it on and to share the review with anyone else that you think could also benefit from it. Also, we realize that details about annuities – and other financial products, too – can and do change somewhat quickly. With that in mind, if you happened to notice anything in this review that needs to be corrected and/or updated, please let us know that as well and we will get on the revisions right away. Are there any other annuities that you would like to see information about? No problem! If you would like to see reviews on any other annuity (or annuities), our team of annuity “geeks” will get on the ball and get them on our website. Just simply click here to let us know which product (or products) you are interested in seeing. And, be sure to check back soon. Best, The Annuity Gator. P.S. If you would like to read more of our MassMutual annuity reviews here are some links to check out:- Independent Review of the Mass Mutual RetireEase Choice QLAC

- Independent Review of the MassMutual RetireEase Immediate Fixed Income Annuity

- Independent Review of the Massachusetts Mutual Stable Voyage 7 Year MYGA Annuity

- Independent Review of the MassMutual RetireEase Choice Deferred Income Annuity (DIA)

- Independent Review of the Massachusetts Mutual Odyssey Select 7 Year MYGA Annuity

- Independent Review of the MassMutual Stable Voyage Fixed Deferred Annuity

- Independent Review of the Massachusetts Mutual Odyssey Select 9 Year MYGA Annuity

- Independent Review of the Massachusetts Mutual Life Stable Voyage 5 Year Single Premium Fixed Deferred Annuity

- Independent Review of the C.M. Life Index Horizons Annuity

- Independent Review of the MassMutual AgeUp Annuity