What will you learn in this annuity review?

This review of the TIAA Traditional Annuity will go over the following information:

- Type of annuity

- Who is eligible

- Pros and cons

- Fees

- Income options

One of the biggest concerns on the minds of retirees today is running out of income. Given our longer life expectancy these days, retirement income may need to be stretched out for 20 or more years. That’s why having a reliable source of lifetime income that arrives regularly – regardless of what is happening in the stock market – can mean the difference between a retirement full of worry, or one of fun and adventure.

As a current or former employee of a non-profit or government organization, you – as well as members of your immediate family – can benefit in retirement with the TIAA Traditional Annuity.

In addition to guaranteed growth (as well as protection of your principal), you can choose an income stream that works for you and your specific needs. This can include the lifetime income option that keeps paying out regardless of how long you may live.

But in return for these benefits, you may have to make some tradeoffs. So, be sure that you know what those are before you give the green light to purchasing this – or for that matter, any – annuity.

Annuity and Retirement Income Planning Information That You Can Trust

If this is the first time you have visited our website, we’d personally like to welcome you to AnnuityGator.com. We are a team of experienced financial pros and retirement income experts who are dedicated to providing you with comprehensive and non-biased annuity reviews.

We have been offering these reviews for quite a few years now – much longer than our competitors have been – and because of this, we have come to be a highly trusted source of annuity information. We have hundreds of reviews in our annuity review database on our website. So, please feel free to spend as much time as you’d like looking over them.

If your search for annuities has been conducted via the Internet, it is likely that you have come across a lot of conflicting details about these products. This isn’t really all that surprising though, as there are a multitude of different annuities in the market today, and there are numerous opinions about them.

Even though there are a number of very good websites that are focused on marketing their annuities online, the reality is that some of these sites will work hard at luring you in by touting some pretty impressive claims, such as:

- Highest income payouts

- Top-rated annuity companies

- Guaranteed income for life

- Lowest annuity fees

Does this look familiar?

Yet, as enticing as these claims may be, you really should treat them as you would when considering any other high-dollar purchase. In other words, you need to make sure that these claims are backed up before you move forward. This can oftentimes require that you look a bit deeper into the “fine print” about the annuity you are considering. That’s where we come in.

If you really want to learn more about the Traditional Annuity from TIAA, then you have landed in the right place. In fact, we dare say that this website is the only place where you can find all of the key details that you need – including both the advantages and the drawbacks – which can be extremely helpful in helping you to make the right decision as to whether or not this annuity is best for you.

Oftentimes, when an insurance or financial salesperson is trying to sell fixed annuities, they will provide a nice and rosy picture of how these products can provide protection of principal, as well as a set rate of return.

However, in doing so, they can also tend to leave out some of the other important facts, which could be considered as drawbacks. (Can you say minuscule return?!) So, before you move a potentially sizeable chunk of your hard-earned retirement savings into this (or any) fixed annuity, you need to ensure that you first have the whole story.

In order to be clear here, we will say that fixed annuities do offer some great benefits – provided that they coincide with your specific financial goals. So, it is essential that you know what you may be getting into, as well as why you are choosing one particular annuity over a myriad of other alternatives that may also be available to you.

So, if you’re ready to begin, let’s go ahead and dive in!

The TIAA Traditional Annuity at a Glance

| Product Name | TIAA Traditional |

|---|---|

| Issuer | TIAA |

| Type of Product | TIAA |

| A.M. Best Rating | A++ |

| Phone Number | (800) 842-2252 |

| Website | https://tiaa.org/ |

Opening Thoughts on the TIAA Traditional Annuity

Ever since the company was founded more than a century ago, TIAA has been on a mission to help their customers reach their financial goals. The company has primarily served the retirement needs of those who work in the medical, academic, cultural, and research fields, and today TIAA boasts more than 5 million customers.

The company is the largest manager of qualified plan stable value assets with approximately $171.1 billion in stable value accumulation values. The company is also the #1 non-for-profit retirement market provider in assets and participant accounts. In 2018 alone, TIAA paid more than $5 billion to retired clients – which includes more than 33,000 annuitants over the age of 90.

TIAA is considered to be strong and stable financially, and able to pay out its policyholders’ claims. As of year-end 2019, TIAA holds more than $1.1 trillion in assets under management (with holdings in more than 50 countries). And, since its founding, TIAA has paid out more than $459 billion in benefits.

In late 2019, TIAA maintains the following ratings:

- A++ from A.M. Best

- AAA from Fitch

- AA+ from S&P

- Aa1 from Moody’s

Given the tremendous about of market volatility, fixed annuities have become more popular over the past dozen years or so. One reason for this is because people don’t want to lose all that they’ve worked for in a market “correction” – especially as they inch closer to retirement.

But, even though fixed annuities have the ability to keep your money safe, the returns are quite low. So, you really need to compare your potential options with regard to growing and protecting your savings, as well as your options for generating a long-term income in retirement.

Before we get into the gritty details, here are some necessary legal disclosures…

This is an independent annuity product review. It is not a recommendation to purchase or to sell an annuity. TIAA has not endorsed this review in any way, nor do we receive any type of compensation for providing this review. This annuity review is meant solely to be an independent review at the request of our readers so that they may see our perspective when breaking down the positives and the negatives of this particular annuity. Prior to committing to the purchase of any type of insurance and/or investment vehicle, it is critical that you do your own due diligence, and that you also talk with a properly licensed professional if you have any questions that relate to your specific situation. All of the names, materials, and marks that have been used in compiling this annuity review are the property of their respective owners.

For additional information on how to compare annuities so that you can decide which may be the best one for you, in order to obtain our free Annuity Buyer’s Guide.

How TIAA Describes the Traditional Annuity

On its website, TIAA describes its Traditional Annuity as a guaranteed annuity that is designed to be a core component of a diversified retirement savings portfolio that can provide you with a solid foundation for retirement.

Contributing to the Traditional Annuity from TIAA can give you the certainty and dependability that you will have a “salary” in retirement. (After all, retirement income is essentially a way to replace your paycheck from your employer).

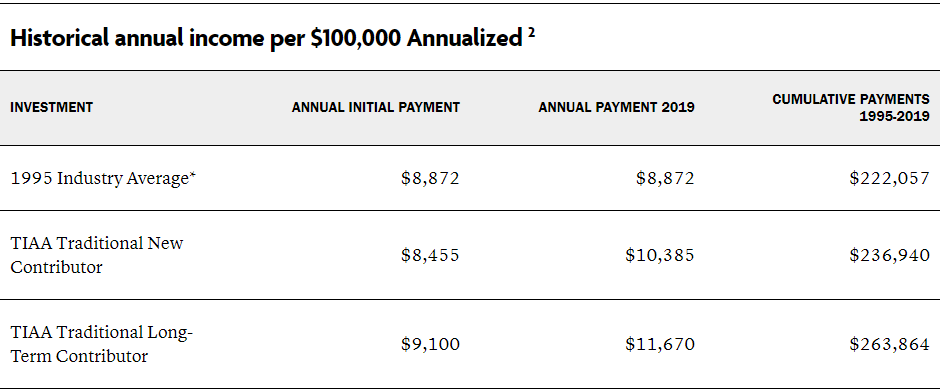

In this Traditional Annuity, your balance grows every day, guaranteed. One of the unique features of the Traditional Annuity is that it can further reward you through the TIAA “sharing the profits” approach.

Even though these payments are not guaranteed, TIAA has historically provided its long-term contributors with higher initial payment(s) and have given their participants increases in their annual income.

For many years, TIAA has rewarded participants who save money in annuity contracts where the benefits are paid in installments over time instead of in an immediate lump sum. The company does this by crediting higher interest rates – typically of between 0.50% and 0.75% – higher.

You can learn more about the TIAA sharing the profits here.

When the time comes to turn on the income stream, you can convert all, or even just some, of the annuity account balance, and leave the rest to continue growing on a tax-deferred basis.

You have the option of setting up a single life income, or alternatively a joint-life option through which you and another individual, such as a spouse or partner, can depend on income throughout the remainder of both lives.

To access the Traditional Annuity information from TIAA’s website, you can go here.

How an Insurance or Financial Advisor Might “Pitch” the TIAA Traditional Annuity

Given all of the guarantees that a fixed annuity like the TIAA Traditional Annuity can provide, it is likely that if you have been presented with this product by an insurance or financial advisor, they touched on the safety of principal, along with the set amount of growth, and the reliability of the income you can receive.

What the advisor might not focus on, though, is the fact that most fixed annuities offer a painfully low rate of return – in some cases in the same neighborhood as CDs and government bonds. So, unfortunately, even though your principal is safe, you would be hard-pressed to meet, much less beat inflation.

Also, if you withdraw more than a certain amount from your account (typically 10% of the contract’s value) during the annuity’s surrender period, you will usually be hit with a surrender penalty. So, taking money out of the annuity can definitely cost you.

The Annuity Gator’s End Take on the TIAA Traditional Fixed Annuity

Where it works best:

Given its safety and income options, the TIAA Traditional annuity will usually work the best for those who are looking for:

- Guaranteed lifetime income

- Safety of principal

- A set rate of interest

- Tax-deferred growth

*Note that not everyone can qualify for this annuity. Current or former employees of non-profit or government organizations can purchase this annuity through a TIAA IRA (as can their immediate family members). It may also be available through non-profit or government employees’ employer-sponsored retirement plans).

Where it works the worst:

This traditional fixed annuity may not be an ideal fit if you:

- Want access to most or all of your funds during the surrender period

- Are seeking a high rate of return on your money

- Do not plan to use the lifetime income feature

In order to know how to really compare the best annuity options for you, so that you can download our free annuity report.

In Summary

There are a lot of important factors that should be considered when you are trying to determine which annuity is right for you – or even if any annuity will fit into your overall financial picture.

In any case, though, annuities should always be considered as long-term financial endeavors, and because of that, you should feel comfortable that an annuity you ultimately go with can help you to reach your goals.

If you are still leaning towards the purchase of a traditional fixed annuity, you can certainly be assured that your principal will be safe and that you will earn a steady, tax-advantaged gain in the account.

However, even with these nice benefits, this annuity could still fall somewhat short – and quite frankly, there very well could be a better option out there for you – particularly if you are focused on getting a guaranteed lifetime income in retirement AND the opportunity to earn a higher rate of return.

If you still have any questions with regard to whether or not the Traditional Annuity from TIAA is right for you – or, even if you just simply need some additional guidance about annuities in general – then please feel free to reach out to us directly via our secure contact form here.

Do You Have Any Additional Questions About the TIAA Traditional Annuity? Did You Notice Any Mistakes in this Annuity Review?

Although this review of the TIAA Traditional Annuity was a bit lengthy, we would much rather provide you with too many details as versus not nearly enough. Therefore, if you did find this review helpful to you, then please feel free to share it with others that you think might benefit, too.

We also understand that annuity product information can change frequently. Therefore, if you happened to notice that any of the information in this annuity review was incorrect, then please let us know and we will do our best to get that updated as soon as possible.

In addition, if this annuity review made this product even more confusing – and/or if it happened to spark any additional questions or concerns – please let us know that, too and we will work to make the information clearer.

Are there any other annuity reviews that you would like to see posted in our annuity review database?

If so, we’ll get on it! Just simply tell us the name of the annuity (or annuities, if more than one) and our highly trained team of annuity “geeks” will start working on those – so be sure to check back soon for updates, as well as a whole host of new annuity reviews!

Best,

The Annuity Gator.

P.S. If you would like to read more of our TIAA annuity reviews here are some links to check out:

- Independent Review of the TIAA Single Premium Immediate Annuity.

- Independent Review of the Intelligent Variable TIAA-CREF Annuity – [Updated January 2020].

4 Comments

Like many who opted for the Guaranteed TIAA Fund, it wasn’t explained to me by my employer, regarding the limitations of withdrawal of what’s in fact my money. The only option is to received a piffling annual amount, and in my case that’s approximately $1500 once a year.

The COVID crises blew off the covers of how Wall Street, Corporate America including TIAA, and Congress & state governments to expose their total disregard poor people. They make billions and billions of $s on our low status in the equation.

All that to say, TIAA, is as much of a bandit organization as the rest. Is there anyway legally to force TIAA to negotiate a full payment option from the Guaranteed Annuity Fund? As if I die (I’m 80 years old) it appears that fund will be null and void regarding any payout.

Can you clarify the above and offer any options for legally forcing TIAA to negotiate the payout process to my advantage while I’m alive and breathing. I just saw the above “Leave a Reply” rather than ask a question. Would someone at least kindly acknowledge my inquiry?

Hi C.E. Walker,

Thank you for your message.

We know annuities can be complex and we would be happy to help you with your inquiry.

We strive to help as many people as we can and we realize that there will be instances where an annuity is not suitable for everyone. We’d be happy to connect you with one of our licensed agents to see if they can assist to resolve any frustrations or questions you might have. Please feel free to reach out to us directly at (888) 440-2468. Or alternatively, you can contact us by going to https://www.annuitygator.com/contact/ and letting us know what time works best for you.

We look forward to chatting with you.

Best,

Annuity Gator

I am currently receiving a TIAA annuity.

When I chose this option, I did not realise that I was PURCHASING it. I thought it is just a way to choose to drawdown my retirement funds. (It is not that large since I left the U.S.A. for New Zealand in 1971.)

If I did purchase it, I was never notified of this fact. I chose to start receiving TIAA annuity payments in 2002, when I turned 65.

What would have been the purchase price for this annuity: TIAA Contract: Y064646-6

Your Auunuitygator article mentions fees, but it never says what these are. Are they annual fees? If so how much.

• One last question. I chose to have a joint annuity with my wife, Eugenie Louise Harris. Sadly, she died Feb. 11, 2020. Do I need to report this to TIAA, and if so, how? Do I need to send a death certificate?

Hi John – Thank you for your message.

We are sorry for your loss. Regarding your inquiry, we would be happy to set up a time to go over an annuity test. This can help you to determine how the annuity is performing for you, and also give a direction for moving forward. In order to provide you with the best advice, we would need to get a bit more information from you. Rather than emailing sensitive details back and forth, though, it would be best to chat via phone. Please feel free to reach out to us directly, toll-free, at (888) 440-2468 to chat with one of our annuity specialists or visit https://www.annuitygator.com/contact/

We look forward to chatting with you.

Best,

Annuity Gator