As interest rates have continued to rise, they are having a tremendous impact on home mortgages and fixed income investments. In the case of the former, rising rates can mean bigger house payments. In the latter, though, you could generate more growth and/or income.

But what could higher interest rates mean for annuities?

The answer to that really depends on the actual annuity you own. So, it is important that you understand how annuities work and what they can (and cannot) do for you before you purchase one.

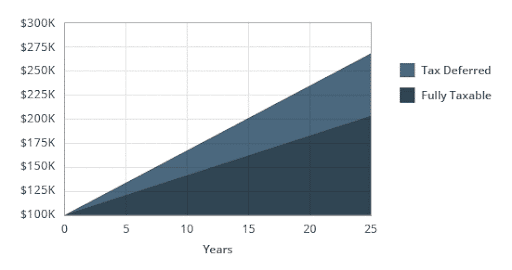

Tax Deferred versus Fully Taxable Growth (with all other factors being equal)

The Effect of Higher Interest Rates on Annuities

Different annuities can be affected in different ways when interest rates rise and fall. For instance, fixed annuities – which are insurance contracts that pay out a pre-set guaranteed interest rate – are typically impacted the most. In this case, if you plan to use the annuity as a retirement income-generating vehicle, you could receive a higher payout. This, in turn, means that you could have more cash flow to use for your essential (and possibly also non-essential) expenses in the future. Fixed indexed annuities (FIAs) are a type of fixed annuity. While there is a fixed account option available with FIAs, these annuities primarily base their return on the performance of one or more underlying market indexes, such as the S&P 500. If the index performs well in a given time period (such as a contract month or year), the annuity is credited with a positive return, oftentimes up to a stated maximum. In return for this limited upside, though, if the underlying index(es) perform poorly, there is generally no loss incurred by the account.Annuities versus Bonds

With rising interest rates affecting both bonds and fixed annuities, it may be difficult to determine which of these financial vehicles is best for you. In doing so, both provide principal protection, and each can provide you with regular income payments. However, there are several areas where a fixed annuity may still come out on top. These can include:- Ongoing payments for life

- Tax-deferred growth

Tax Deferred versus Fully Taxable Growth (with all other factors being equal)

Is an Annuity Right for You in a Rising Interest Rate Environment?

There are many factors that you should take into consideration before you purchase an annuity. These can include your age, risk tolerance, and time frame until retirement. In addition, if you are leaning towards an annuity to supplement your retirement income, you should also consider other income sources that you may have, such as Social Security and/or an employer-sponsored pension plan. There are many different types of annuities available in the marketplace today, and they can often have many “moving parts.” With that in mind, it can help if you discuss your options with a specialist in retirement income planning. That’s where Annuity Gator comes in. We are a team of annuity and retirement income experts who have a key focus on ensuring that you don’t have any “gaps” in your future cash flow stream, while at the same time keeping your portfolio protected. If you would like to set up a time to talk with an annuity specialist, please feel free to contact us via phone at (888) 440-2468 or by email by going to our secure online contact form. We look forward to hearing from you.