What We Will Be Covering in this Annuity Review

In this annuity review, we will be going over the details regarding the Athene Balanced Choice Level 10 fixed indexed annuity, such as:- Product type

- Fees

- Current rates

- Realistic long-term return expectations

- How it is used

- How it is most poorly used

Annuities can be complex. That’s where having an Annuity Investigator who loves math comes in. We make the complex, simple.

If you’ve been tossing around the idea of purchasing an annuity because you are seeking additional tax-deferred growth, protection of principal (in any market environment), and a lifetime income stream, then the Balanced Choice Level 10 annuity from Athene could be a good option for you. That’s because this fixed indexed annuity can allow you to protect the money you’ve worked for and attain the upside of the market, while at the same time not forcing you to settle for low-interest rates. But, prior to making a long-term commitment to this – or to any – financial vehicle, there are some things that you should know that could have a big impact on whether or not it is the right choice. Over the past several years, fixed indexed annuities have become quite popular – particularly with those who are seeking higher returns than what a regular fixed annuity can give, yet also want the principal protection of their hard-earned savings. Fixed indexed annuities can provide all of this – as well as a lifetime income in retirement. However, because these types of annuities have become so in dement, many insurance carriers have expanded their product lines and have added all kinds of “bells and whistles” to them. And, while this can be beneficial, it can also make an already confusing product even more so – and, many of these product add-ons will cost you an additional amount of premium, in turn, negatively impacting the ultimate benefit that you end up with. Although this may not necessarily be bad in all cases, it is important that you at least know how the product works and what it will cost – and then determine whether or not you want to move forward with it.

Annuity and Retirement Income Planning Information You Can Trust

If you have never been to our website before, please allow us to officially welcome you here to AnnuityGator.com. We are a team of annuity experts who have a primary focus on providing highly comprehensive, and unbiased, annuity reviews online. We have been doing this for quite a long time now – far longer than our competitors have – and because of that, we have come to be known as a highly trusted source of annuity information. We’ve also had some “copycats” try to duplicate our offerings. The way we see this, though, is that imitation is surely the highest form of flattery. If you have been in the process of seeking an annuity, it is likely that when doing any research online about them, you have come across some highly conflicting details. This really is not all that surprising, though, as there are a lot of annuities available in the market today, and there are many opinions, both positive and negative, about them. You may also have attended an annuity seminar or workshop where the presenter offered you a free dinner or lunch, as well as information regarding the Athene Balanced Choice Level 10 fixed indexed annuity, or some other similar product. Your attendance at that seminar or workshop might even be the catalyst that has ultimately led you here to our site. That being said, although there are many other good websites out there online that are focused on annuities, you may have found in your quest for information that some of these websites will try luring you in by making some fairly bold claims, like having the lowest fees and offering the highest annuity income payouts. Sound familiar? But, even though these claims might sound really enticing, the reality is that prior to you making a commitment on an annuity, it is important for you to find out whether or not these claims are really true, just as you would do prior to purchasing any other high-dollar item. This is where the Annuity Gator comes in! If your intention is to learn more about the Balanced Choice Level 10 Annuity from Athene, then the good news is that you are in the right place. In fact, we dare say that our website is the only place on the Internet where you can find all of the in-depth details about this annuity – which includes the good, and the bad. That’s because we feel that knowing the whole story about an annuity is the only way for consumers to make a truly well-informed decision about whether or not it is the right product for them. Oftentimes, when a financial or insurance advisor is presenting a fixed indexed annuity to his or her clients, they will provide a nice rosy picture of how the annuity can offer the best of all world, meaning that the product has the ability to offer a nice return, along with safety of principal – as well as income for life. But in doing so, the advisor may neglect to provide details about areas that could be considered drawbacks. With that in mind, if you are considering moving forward with the purchase of the Athene Balanced Choice Level 10 annuity, you really need to know what it is that you’re getting into. A primary reason for this is because getting out of an annuity can be somewhat difficult – as well as very expensive, due to the surrender charges that are incurred. Just to be completely clear here, we do want to state that we feel annuities can be a good financial vehicle for many investors – as long as it fits in well with both their short- and long-term financial goals. So, if you’re ready to begin this review, let’s go ahead and dive in!Athene Balanced Choice Level 10 Annuity at a Glance

| Product Name | Balanced Choice Level 10 |

|---|---|

| Issuer | Athene |

| Type of Product | Fixed Indexed Annuity |

| S&P Rating | A- (Strong) |

| Phone Number | (888) 266-8489 |

| Website | https://www.athene.com |

Opening Thoughts on the Athene Balanced Choice Level 10 Annuity

Athene USA is a somewhat newer name for an acquisition of a long-established life insurance carrier that has a century-old track record in the insurance and financial services industry. This company’s life insurance offices are based out of Delaware, Iowa, and New York. Athene USA services customers in all 50 of the United States. Athene is one of the fastest growing providers of indexed annuities. As of year-end 2017, Athene held nearly $100 billion in total GAAP assets. The company also held approximately 815,000 insurance policies in force, and it has earned high ratings from the top insurer rating agencies. These include an A- (Strong) from S&P, an A (Excellent) from A.M. Best, and an A- (Strong) from Fitch. Throughout the past decade or so, the volatility in the market has made investors think twice about putting their hard earned savings into an area that could wipe away years of planning within a very short time if experiencing a correction. Yet at the same time, historically low-interest rates have not provided investors anywhere near the returns they need in order to beat – or even meet – future inflation. This is where the fixed indexed annuity can come in. These financial vehicles allow you the opportunity to attain index-linked returns as well as the safety of principal, regardless of what occurs in the market. Just like other types of annuities, these products also offer tax-deferred earnings within the account – and, there is the option to receive a lifetime income in retirement, regardless of how long you may need it. However, even though this “best of all worlds” scenario initially seems very appealing, these benefits can also come at a cost. So, before you move forward with the purchase of the Destination fixed indexed annuity (or for that matter, any annuity), you need to be sure that you check out all of the details as, once you have purchased an annuity, it could be quite an ordeal to get yourself out of it.Before getting into the nitty-gritty details, here are some necessary legal disclosures…

This is an independent annuity product review. It is not a recommendation to purchase or to sell an annuity. Athene has not endorsed this review in any way, nor do we receive any type of compensation for providing this review. This annuity review is meant solely to be an independent review at the request of our readers so that they may see our perspective when breaking down the positives and the negatives of this particular annuity. Prior to committing to the purchase of any type of insurance and/or investment vehicle, it is critical that you do your own due diligence, and that you also talk with a properly licensed professional if you have any questions that relate to your specific situation. All of the names, materials, and marks that have been used in compiling this annuity review are the property of their respective owners. For additional information on how to compare fixed annuities so that you can decide which may be the best one for you, click here in order to obtain our free annuity report.How Athene Describes the Balanced Choice Level 10 Annuity

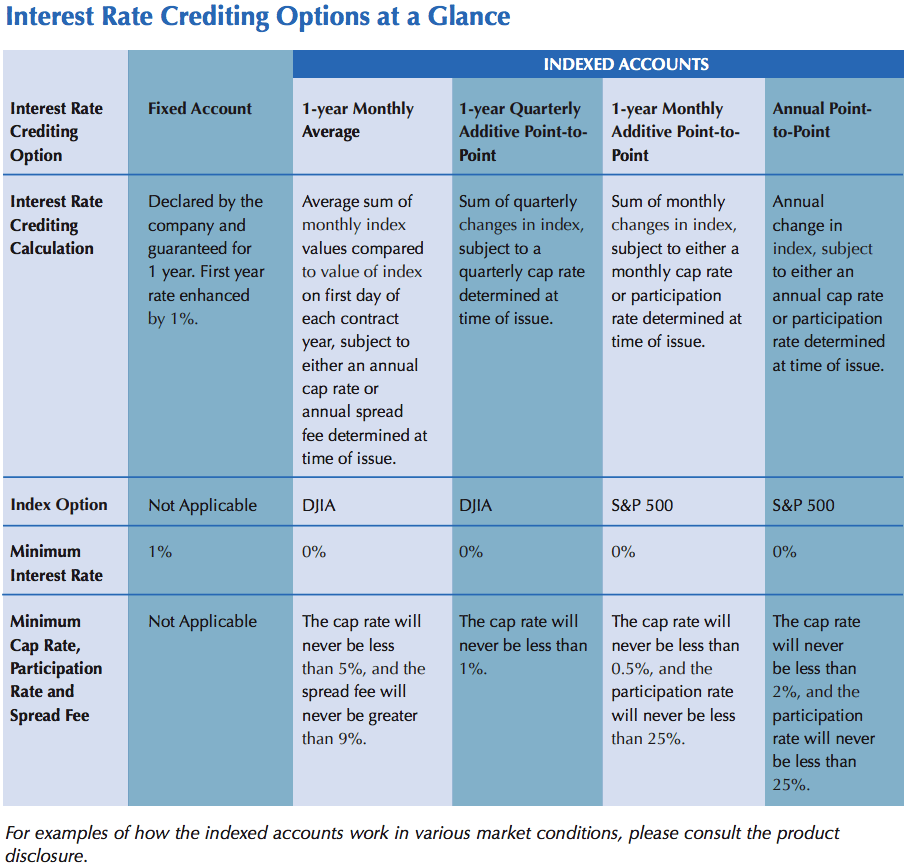

The Balanced Choice annuity series by Athene offer a balanced allocation strategy that put a key focus on flexibility and growth. The Level 10 Balanced Choice annuity has a ten year surrender period – so it should definitely be considered as a longer-term financial endeavor. In addition to the index crediting, the Balanced Choice Level 10 also offers a fixed rate option, which offers a guaranteed rate (note, though, that this interest rate may change at the beginning of each contract year). This annuity also offers some additional bells and whistles, such as a death benefit, along with an optional death benefit rollup. There is also a lifetime income rider that can provide you (and your spouse, if applicable) with guaranteed income for life.

To check out all of the company-specific details, you can find the product brochure HERE.

This annuity also offers some additional bells and whistles, such as a death benefit, along with an optional death benefit rollup. There is also a lifetime income rider that can provide you (and your spouse, if applicable) with guaranteed income for life.

To check out all of the company-specific details, you can find the product brochure HERE.

How a Financial or Insurance Professional May “Pitch” this Product to You

Fixed indexed annuities can offer some very nice advantages – starting with the fact that they allow the opportunity to get a higher return than a regular fixed annuity, and still protect your principal in any type of market environment. As with other annuities, your earnings can compound tax-deferred, so you can continue to build the funds in the account without the need to pay Uncle Sam each year (until the time of withdrawal). These products also allow you to get income for life, so you can alleviate the worry about running out of income in retirement. With that in mind, a financial advisor is likely to focus on this “best of all worlds” scenario when presenting this product to you. However, because there are so many moving parts on fixed indexed annuities, you really need to take a deeper look into how the components of these annuities work because typically, they aren’t always a walk in the park when it comes to generating the returns you are anticipating. For example, many fixed indexed annuities – including this one – come with a cap on the index-related / credited earnings. This means that should the underlying index that is being tracked have an absolutely stellar performance during a given year, your return will be capped, or limited, based on what the insurance company has set the cap rate at. (So much for those regular 7 – 8% annual earnings the other websites told you about!) In addition to possible surrender charges, there can also be some fees involved if you own the Athene Balanced Choice Level 10 fixed indexed annuity.Fees Associated with the Athene Balanced Choice Level 10 Fixed Indexed Annuity

When you have a financial product that offers any type of guarantee on it, it’s likely that there will also be tradeoffs to consider somewhere along the line. This definitely holds true with the Athene Balanced Choice Level 10 fixed indexed annuity – and several of these tradeoffs come in the form of fees. Here, while partial withdrawals are always available, a contract charge will be assessed on the portion of that withdrawal that exceeds the free withdrawal privilege amount, or if the annuity is completely surrendered early. The amount of these fees start at either 10% or 9%, depending on your state of residence, and they gradually grade down over a period of 10 full years as follows:Surrender Charges for All Approved States Except CA, TX, and WA

| Contract Year | Charge % |

|---|---|

| 1 | 10 |

| 2 | 10 |

| 3 | 9.5 |

| 4 | 9 |

| 5 | 8 |

| 6 | 7 |

| 7 | 6 |

| 8 | 5 |

| 9 | 4 |

| 10 | 2 |

| 11+ | 0 |

Surrender Charges for California, Texas, and Washington

| Contract Year | Charge % |

|---|---|

| 1 | 9 |

| 2 | 9 |

| 3 | 8 |

| 4 | 7 |

| 5 | 6 |

| 6 | 5 |

| 7 | 4 |

| 8 | 3 |

| 9 | 2 |

| 10 | 1 |

| 11+ | 0 |

The Annuity Gator’s End Take on the Athene Balanced Choice Level 10 Fixed Indexed Annuity

Where it works the best: This annuity could work for you if you are looking for:- Safety of your principal – regardless of what occurs in the market

- The opportunity for index-linked growth

- Guaranteed lifetime income in retirement

- Want penalty-free access to most or all of your money within the first ten full years of purchasing the annuity

- Do not intend to use the lifetime income feature of the annuity

In Summary

There are many different factors that you should consider prior to making a long-term commitment to purchasing an annuity. For example, in addition to knowing that it can be costly to change your mind, you should also consider why you may be choosing one fixed indexed annuity over a long list of other products that may also suit your particular financial needs. When considering the Athene Balanced Choice Level 10 Fixed Indexed Annuity, you can be confident that the principal you have in the account is safe, regardless of what happens in the market – or even in the economy overall. You can also be sure that you will have an income in retirement for as long as you (and your spouse, if applicable) need it. However, that being said, this annuity could also fall somewhat short – and there could be some other, better alternatives that are available to you. But even so, the only way to really know if this annuity is right for you is to have it tested. We can assist you with that by running it through our annuity calculator, using your particular financial figures. If this is something that would be of interest to you, then please contact us.Do You Have Any More Questions About this Annuity? Did You Notice Any Mistakes in this Review?

We realize that this annuity review ran a tad bit on the long side, however, we feel that providing you with “too much” information is far better than not giving you enough. So, if you felt that this review was helpful, please feel free to pass it along and share it with anyone else whom you think could also benefit from it. In addition, we also realize that the information about annuities can – and often does – change. Therefore, if you happened to notice if there were any details within this review that should be revised, please let us know that too, and we will be glad to make the necessary updates to it. Are there any other annuities that you would like to know more about? If so, just let us know the name (or names) of the annuity(ies) and our AnnuityGator annuity “geeks” will get on it. So, be sure to check back soon and regularly to see all of our new and updated annuity reviews. Best, The Annuity Gator P.S If you would like to read more of our Athene annuity reviews here are some links to check out.- Athene Balanced Choice Annuity (BCA) Elevate Fixed Indexed Annuity

- Athene Ascent Fixed Indexed Annuity

- Athene Ascent 10 Bonus Fixed Index Annuity

- Athene Income Select Bonus Fixed Index Annuity

- Athene Ascent 10 Bonus 2.0 Fixed Indexed Annuity with Ascent Income Rider Option 1

- Athene MYG 5 Fixed Annuity

- Athene MaxRate 7 Multi-Year Guarantee Annuity

- Athene Ascent Accumulator 10 Fixed Indexed Annuity

Donna Michals

This sentence contained the word “dement” which I was not familiar with and looked it up and found it is a word that references someone with dementia. I can only assume the word was meant to be “demand”. When researching information as important as this I lose interest as soon as I see this type of mistake. This was part of the first paragraph of this article.

However, because these types of annuities have become so in dement, many insurance carriers have expanded